425: Filing under Securities Act Rule 425 of certain prospectuses and communications in connection with business combination transactions

Published on August 19, 2021

Filed by Arqit Quantum Inc.

Pursuant to Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

under the Securities Exchange Act of 1934

Subject Company: Centricus Acquisition Corp. (Commission File No. 001-39993)

Commission File No. for the Related Registration Statement: 333-256591

Arqit Stronger simpler encryption August 2021

2 Disclaimer (1/2) The following presentation, the information communicated during any delivery of the presentation and any question and answer ses sion and any other materials distributed at or in connection with the presentation (collectively, this “presentation”) has be en prepared by Arqit Quantum Inc. (“Arqit”) and Centricus Acquisition Corp. (“Centricus”) in connection with a proposed business combination betwe en Arqit and Centricus (the “Transaction”) and for no other purpose. This presentation may not be reproduced or distributed, in wh ole or in part. No Representations and Warranties This presentation is for informational purposes only and does not purport to contain all of the information that may be requi red to evaluate the Transaction. This presentation is not intended to form the basis of any investment decision and does not cons ti tute investment, tax or legal advice. No representation or warranty, express or implied, is or will be given by Arqit or Centricus or any of thei r r espective affiliates, directors, officers, employees or advisers or any other person as to the accuracy or completeness of th e i nformation in this presentation or any other written, oral or other communications transmitted or otherwise made available to any party in the c our se of its evaluation of a possible transaction between Arqit and Centricus and no responsibility or liability whatsoever is a cce pted for the accuracy or sufficiency thereof or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. The informat ion contained in this presentation is preliminary in nature and is subject to change, and any such changes may be material. Arqit a nd Centricus disclaim any duty to update the information contained in this presentation. Viewers of this presentation should each make th eir own evaluation of Centricus, Arqit and the Transaction and of the relevant and adequacy of the information contained herein a nd should make such other investigations as they deem necessary. Forward - Looking Statements This presentation includes “forward - looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Arqit’s and Centricus’ actual results may differ from their expectations, e sti mates and projections and consequently, you should not rely on these forward - looking statements as predictions of future events. Words such as “expec t”, “estimate”, “project”, “budget”, “forecast”, “anticipate”, “intend”, “plan”, “may”, “will”, “could”, “should”, “believes” , “ predicts”, “potential”, “continue”, and similar expressions are intended to identify such forward - looking statements. These forward - looking statements include, without limitation, Arqit’s and Centricus’ expectations with respect to future performance and anticipated financial im pacts of the Transaction, the satisfaction of closing conditions to the Transaction and the timing of the completion of the Transaction. The se forward - looking statements involve significant risks and uncertainties that could cause the actual results to differ material ly from the expected results. Most of these factors are outside Arqit’s and Centricus’ control and are difficult to predict. Factors that may ca use such differences include, but are not limited to: (1) the outcome of any legal proceedings that may be instituted against Ar qi t or Centricus following the announcement of the Transaction; (2) the inability to complete the Transaction, including due to the inability to concurr ent ly close the business combination and the private placement of common stock or due to failure to obtain approval of the stock hol ders of Centricus; (3) delays in obtaining, adverse conditions contained in, or the inability to obtain necessary regulatory approvals or comple te regular reviews required to complete the Transaction; (4) the risk that the Transaction disrupts current plans and operations as a result of the announcement and consummation of the Transaction; (5) the inability to recognize the anticipated benefits of the Transaction, wh ich may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profit abl y, maintain relationships with customers and suppliers and retain its key employees; (6) costs related to the Transaction; (7) changes in th e applicable laws or regulations; (8) the possibility that the combined company may be adversely affected by other economic, bus iness, and/or competitive factors; (9) the impact of the global COVID - 19 pandemic: and (10) other risks and uncertainties indicated from time to time described in Centricus’ registration statement on Form S - 1, the proxy statement relating to the Transaction, including t hose under “Risk Factors” therein, and in Centricus’ other filings with the U.S. Securities and Exchange Commission (“SEC”). Arqit and Centric us caution that the foregoing list of factors is not exclusive and not to place undue reliance upon any forward - looking statements, including projections, which speak only as of the date made. Neither Arqit nor Centricus undertakes or accepts any obligation to relea se publicly any updates or revisions to any forward - looking statements to reflect any change in its expectations or any change in e vents, conditions or circumstances on which any such statement is based. Industry and Market Data In this presentation, Arqit and Centricus rely on and refer to publicly available information and statistics regarding market pa rticipants in the sectors in which Arqit competes and other industry data. Any comparison of Arqit to the industry or to any of its competitors is based on this publicly available information and statistics and such comparisons assume the reliability of the information availabl e t o Arqit. Arqit obtained this information and these statistics from third - party sources, including reports by market research fi rms and company filings. While Arqit believes such third - party information is reliable, there can be no assurance as to the accuracy or completeness of t he indicated information. Neither Arqit nor Centricus has independently verified the information provided by the third - party so urces. Trademarks This presentation may contain trademarks, service marks, trade names and copyrights of other companies, which are the propert y o f their respective owners. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referre d t o in this presentation may be listed without the TM, SM © or © symbols, but Arqit and Centricus will assert, to the fullest extent unde r a pplicable law, the rights of the applicable owners, if any, to these trademarks, service marks, trade names and copyrights. No Offer or Solicitation This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitati on of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or s ale would be unlawful prior to the registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made exc ept by means a prospectus meeting the requirements of Section 10 of the Securities Act, or an exemption therefrom.

3 Disclaimer (2/2) Use of Projections This presentation also contains certain financial forecasts, including projected revenue, gross profit, EBITDA and unlevered fre e cash flow (“uFCF”) for Arqit’s fiscal years 2021 through 2025. Neither Centricus’ nor Arqit’s independent auditors have au dit ed, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, an d accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purp ose of this presentation, These projections are for illustrative purposes only and should not be relied upon as being necessarily indicat ive of future results. In this presentation, certain of the above - mentioned projected information has been provided for purposes o f providing comparisons with historical data. The assumptions and estimates underlying the prospective financial information are inheren tly uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that co ul d cause actual results to differ materially from those contained in the prospective financial information. Projections are inherently uncer tai n due to a number of factors outside of Centricus’ or Arqit’s control. Additionally, the projections are based on current bu sin ess plans and if new business plans are developed and/or implemented there is no assurance that the projections presented herein will be applicabl e. Accordingly, there can be no assurance that the prospective results are indicative of future performance of the combined comp an y after the Transaction or that actual results will not differ materially from those presented in the prospective financial information. In clusion of the prospective financial information in this presentation should not be regarded as a representation by any perso n t hat the results contained in the prospective financial information will be achieved. Use of Non - GAAP Financial Measures This presentation includes certain projections of non - GAAP financial measures, such as EBITDA (and related measures), and certai n ratios and other metrics derived therefrom. Arqit believes that these non - GAAP measures are useful to investors for two princ ipal reasons: 1) these measures may assist investors in comparing performance over various reporting periods on a consistent basis b y removing from operating results the impact of items that do not reflect core operating performance: and 2) these measures are used by Arqit’s management and board of directors to assess its performance and may (subject to the limitations described below) enab le investors to compare the performance of Arqit and the combined company to its competition. Arqit believes that the use of the se non - GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends. These n on - GAAP financial measures are not measures of financial performance in accordance with GAAP and may exclude items that are sign ificant in understanding and assessing Arqit’s financial results. Therefore, these non - GAAP measures should not be considered in isolation from, or as an alternative to, financial measures determined in accordance with GAAP. Due to the forward - looking nature of thes e non - GAAP financial measures, a reconciliation of non - GAAP financial measures in this presentation to the most directly comparable GAAP fi nancial measures is not included, because, without unreasonable effort, Arqit is unable to predict with reasonable certainty the amount or timing of non - GAAP adjustments that are used to calculate these forward - looking non - GAAP financial measures. The non - GAAP finan cial measures included in this presentation may not be comparable to similarly - titled measures presented by other companies. Ce rtain monetary amounts, percentages and other figures included in this presentation have been subject to rounding adjustments. Cert ain other amounts that appear in this presentation may not sum due to rounding. Additional Information Arqit has filed a definitive proxy statement / prospectus with the SEC on Form F - 4 relating to the Transaction, has been mailed to Centricus’ shareholders. This presentation does not contain all the information that should be considered concerning the T ran saction and is not intended to form the basis of any investment decision or any other decision in respect of the Transaction. Centricus’ shareho lde rs and other interested persons are advised to read the proxy statement / prospectus and amendments and supplements thereto, and other documents filed in connection with the Transaction, as these materials contain important information about Arqit, Centricus, and the Transaction. The proxy statement / prospectus and other relevant materials for the Transaction have been mailed to shareh ol ders of Centricus as of the record date, July 26, 2021. Shareholders are also be able to obtain copies of the definitive proxy statem ent / prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a request to Arqit at 3 More London, London SE1 2RE or to Centricus at Centricus Acquisition Corp., Boundary Hall, Cricket Squ are , PO Box 1093, Grand Cayman KY1 - 1102, Cayman Islands. Participants in the Solicitation Centricus and its directors and executive officers may be deemed participants in the solicitation of proxies from Centricus’ sha reholders with respect to the Transaction. A list of the names of those directors and executive officers and a description of th eir interests in Centricus is contained in Centricus’ Registration Statement on Form S - 1, as effective on February 3, 2021, which was filed with the SEC and is available free of charge at the SEC’s web site at www.sec.gov, or by directing a request to Centricus at Centr icu s Acquisition Corp., Boundary Hall, Cricket Square, PO Box 1093, Grand Cayman KY1 - 1102, Cayman Islands. Additional information regarding the i nterests of such participants will be contained in the proxy statement / prospectus for the Transaction when available. Arqit and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the sha reholders of Centricus in connection with the Transaction. A list of the names of such directors and executive officers and i nfo rmation regarding their interests in the Transaction will be included in the proxy statement / prospectus for the Transaction when available.

Centricus Acquisition Corporation overview 4 ▪ Centricus Acquisition Corporation (NASDAQ: CENHU) is a Nasdaq - listed blank check company led by former executives at Silversea Cruises and Centricus ▪ This entity was formed by Centricus and Heritage Group: ▪ Monaco - based private equity group with a core focus / expertise on travel and leisure, technology as well as medical / BioTech companies ▪ London - based global investment firm, overseeing $30bn of assets and targeting returns in four core sectors: Financial services, Technology, Infrastructure and CMES (1) ▪ In February 2021, the company priced an upsized IPO worth $345m by offering 34.5m units at $10.00 per unit Defensible market position in large / growing markets x Compelling upside unlocked through their operational expertise x Forefront of shifting technological and consumer landscapes x Ranging from $1bn – 3bn in transaction value x Garth Ritchie CEO Over 25 years of experience in banking and finance, most recently as the Head of Investment Bank for Deutsche Bank until July 2019, and member of the Board from January 2016. Joined Centricus in June 2020 Manfredi Lefebvre d’Ovidio Chairman Chairman of Heritage Group, and also Executive Chairman from 2001 to 2020 for Silversea Cruises, expanding the company from a cruise line with three vessels to covering over 900 destinations globally Appointed CIO of Heritage Group in 2019, serving as the Managing Director of Silversea Expeditions, Vice Chairman of Abercrombie & Kent, and Chairman of Bucksense Independent director with Altair Partners Limited since May 2018. From October 1994 to June 2017, Nicholas Taylor served at Ashburton Investments, initially as Finance Director before becoming CFO and COO ¹ Consumer, Media, Entertainment and Sports; Source: Company information Cristina Levis CFO, CIO, Secretary Nicholas Taylor Board of Directors Highly experienced management Well defined acquisition criteria Business at a glance

Vision Our mission is to use our world leading quantum encryption platform to keep safe the data of our governments, enterprises and citizens. 5 Arqit’s quantum tech stack allows lightweight end point software to create encryption keys which are computationally secure, zero trust and one time in infinite numbers and infinite group sizes. We already taking the software to market at pace.

Problem: legacy encryption is obsolete 6 ▪ PKI was designed decades ago ▪ It was never intended to protect our hyper connected world ▪ It has many vulnerabilities in its implementation for attackers to exploit ▪ Quantum computers will soon compromise the mathematics at the heart of PKI ▪ The world is being urged to create and adopt new protections ▪ The efforts to make PKI more resistant to quantum attack are temporary, and pose grave problems in usability “We need to determine where, why, and with what priority vulnerable public - key algorithms will need to be replaced, and we need to understand the constraints that apply to specific use cases. These initial steps in developing and implementing algorithm migration playbooks can and should begin immediately.” National Institute of Science and Technology, U.S. Department of Commerce, April 28 th 2021

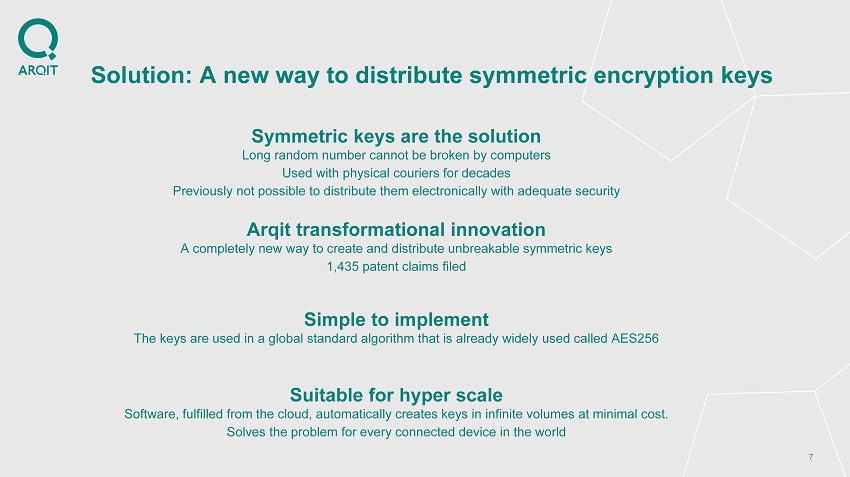

7 Solution: A new way to distribute symmetric encryption keys Arqit transformational innovation A completely new way to create and distribute unbreakable symmetric keys 1,435 patent claims filed Symmetric keys are the solution Long random number cannot be broken by computers Used with physical couriers for decades Previously not possible to distribute them electronically with adequate security Suitable for hyper scale Software, fulfilled from the cloud, automatically creates keys in infinite volumes at minimal cost. Solves the problem for every connected device in the world Simple to implement The keys are used in a global standard algorithm that is already widely used called AES256

8 Transatlantic leadership in cloud encryption David Bestwick CTO & Founder Former CTO, Avanti plc. Marconi engineer. Astrophysicist. Royal Aeronautical Society medal winner Dr Daniel Shiu Chief Cryptographer Former Head of Mathematics & National Technical Authority for Cryptographic Design & Quantum Information Processing, GCHQ Inventor of SSL, Security CTO Sales Force, Operating Partner, Evolution Equity Partners Dr Taher Elgamal Director, Arqit Ltd Former Engineering Director, McAfee UK Enterprise Data Protection David Webb Chief Engineer Former Deputy Chief of Staff for Intelligence, Surveillance, Reconnaissance, and Cyber Effects Operations, U.S. Air Force General VeraLinn Jamieson Director, Arqit Inc Former Chief of Research and Innovation, GCHQ and the Deputy Chief Scientific Advisor for National Security Daryl Burns Inventor, Consultant Former Group CISO, HSBC & CTO, Cisco. PhD Cryptography. Fellow Royal Academy of Engineering Dr Alison Vincent Adviser 44 years’ experience since winning the IBM prize aged 13 specialising in High Performance Computing Dr Barry Childe Chief Innovation officer Former Chief Executive, GCHQ Sir Iain Lobban Adviser Formerly 22 Years a Main Board Director at GCHQ. PhD in Quantum Molecular Dynamics Dr Geoffrey Taylor, CB Co - Founder, Adviser David Williams CEO & Founder Former CEO & Co - Founder, Avanti plc. TMT Banker. Queens Award for Exports 2016 Nick Pointon CFO Former CFO, Privitar. Ex VP Finance, King Digital. KPMG ACA Former four - star Vice Chief of Staff of the US Air Force. Retired 2020 Gen Seve Wilson Director, Arqit Inc Air Vice Marshal RAF Capability, highly decorated aviator & military leader Air Vice Marshal Rocky Rochelle CB COO Former Director, Jumo World and Avanti Government Services. British Army Officer who led the UK’s Counter Terrorism Planning for 2012 Olympic Games Paul Feenan Chief Revenue Officer Formerly of IBM and Hewlett Packard. PhD in Post Quantum Cryptography Stephen Holmes Chief Product Officer

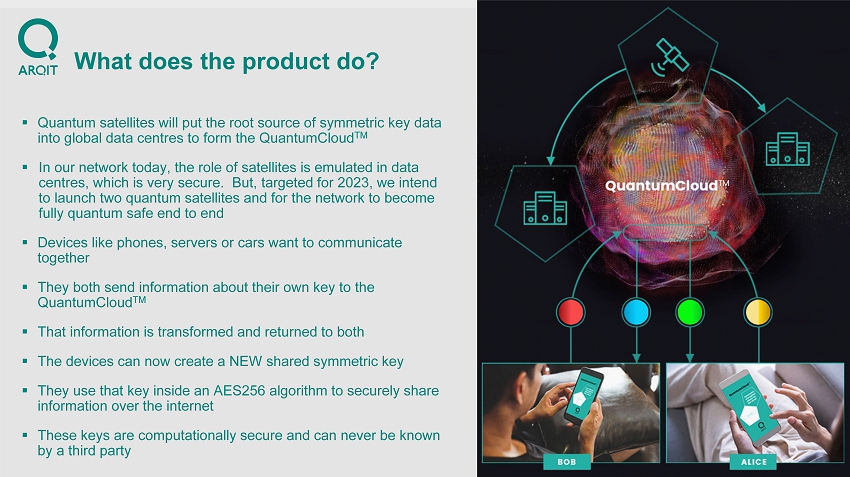

9 What does the product do? ▪ Quantum satellites will put the root source of symmetric key data into global data centres to form the QuantumCloud TM ▪ In our network today, the role of satellites is emulated in data centres, which is very secure. But, targeted for 2023, we intend to launch two quantum satellites and for the network to become fully quantum safe end to end ▪ Devices like phones, servers or cars want to communicate together ▪ They both send information about their own key to the QuantumCloud TM ▪ That information is transformed and returned to both ▪ The devices can now create a NEW shared symmetric key ▪ They use that key inside an AES256 algorithm to securely share information over the internet ▪ These keys are computationally secure and can never be known by a third party

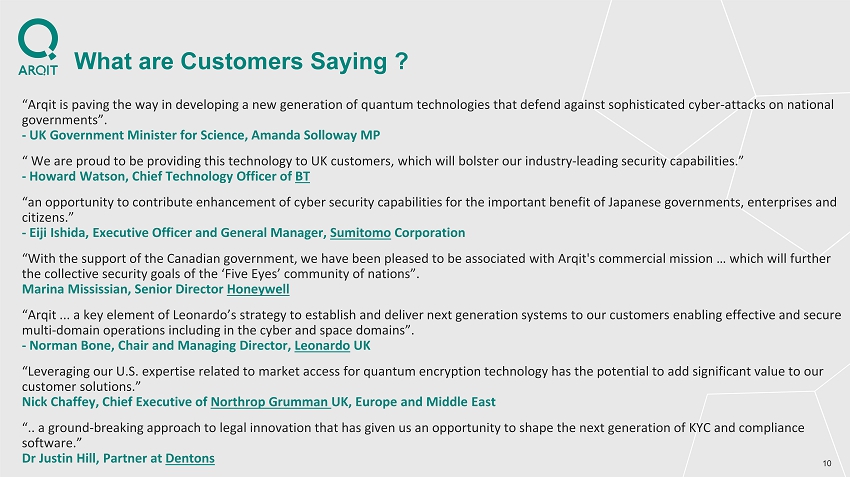

“Arqit is paving the way in developing a new generation of quantum technologies that defend against sophisticated cyber - attacks on national governments”. - UK Government Minister for Science, Amanda Solloway MP “ We are proud to be providing this technology to UK customers, which will bolster our industry - leading security capabilities.” - Howard Watson, Chief Technology Officer of BT “an opportunity to contribute enhancement of cyber security capabilities for the important benefit of Japanese governments, e nte rprises and citizens.” - Eiji Ishida, Executive Officer and General Manager, Sumitomo Corporation “With the support of the Canadian government, we have been pleased to be associated with Arqit's commercial mission … which w ill further the collective security goals of the ‘Five Eyes’ community of nations”. Marina Mississian, Senior Director Honeywell “Arqit ... a key element of Leonardo’s strategy to establish and deliver next generation systems to our customers enabling ef fec tive and secure multi - domain operations including in the cyber and space domains”. - Norman Bone, Chair and Managing Director, Leonardo UK “Leveraging our U.S. expertise related to market access for quantum encryption technology has the potential to add significan t v alue to our customer solutions.” Nick Chaffey, Chief Executive of Northrop Grumman UK, Europe and Middle East “.. a ground - breaking approach to legal innovation that has given us an opportunity to shape the next generation of KYC and complian ce software.” Dr Justin Hill, Partner at Dentons 10 What are Customers Saying ?

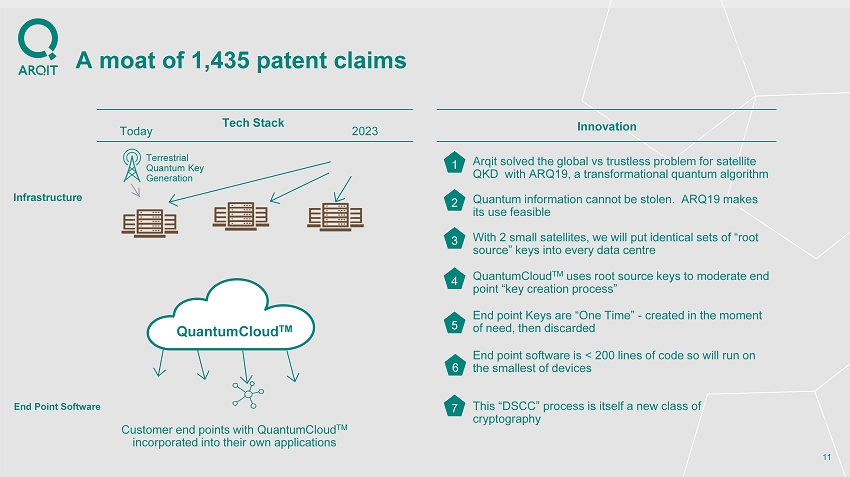

A moat of 1,435 patent claims 11 Today Innovation Arqit solved the global vs trustless problem for satellite QKD with ARQ19, a transformational quantum algorithm 1 4 QuantumCloud TM uses root source keys to moderate end point “key creation process” 5 End point Keys are “One Time” - created in the moment of need, then discarded 6 Customer end points with QuantumCloud TM incorporated into their own applications QuantumCloud TM Quantum information cannot be stolen. ARQ19 makes its use feasible 2 Infrastructure End Point Software With 2 small satellites, we will put identical sets of “root source” keys into every data centre 3 This “DSCC” process is itself a new class of cryptography 7 Terrestrial Quantum Key Generation Tech Stack 2023 End point software is < 200 lines of code so will run on the smallest of devices

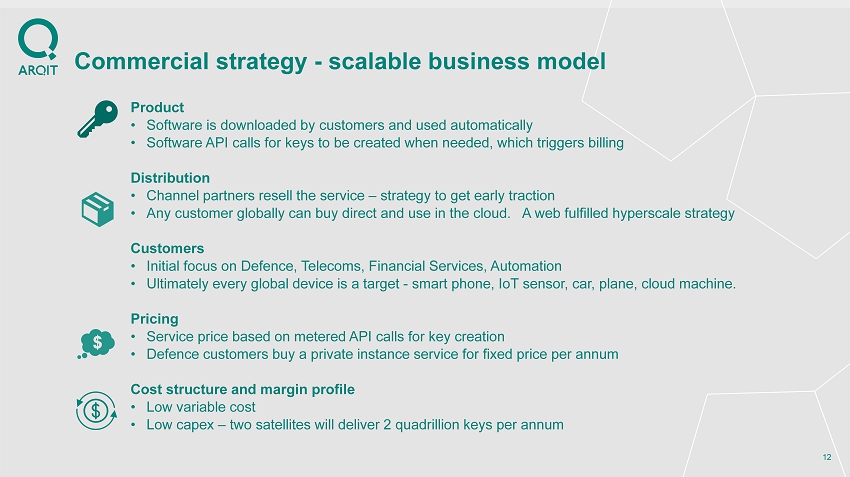

Commercial strategy - scalable business model 12 Product • Software is downloaded by customers and used automatically • Software API calls for keys to be created when needed, which triggers billing Distribution • Channel partners resell the service – strategy to get early traction • Any customer globally can buy direct and use in the cloud. A web fulfilled hyperscale strategy Customers • Initial focus on Defence, Telecoms, Financial Services, Automation • Ultimately every global device is a target - smart phone, IoT sensor, car, plane, cloud machine. Pricing • Service price based on metered API calls for key creation • Defence customers buy a private instance service for fixed price per annum Cost structure and margin profile • Low variable cost • Low capex – two satellites will deliver 2 quadrillion keys per annum

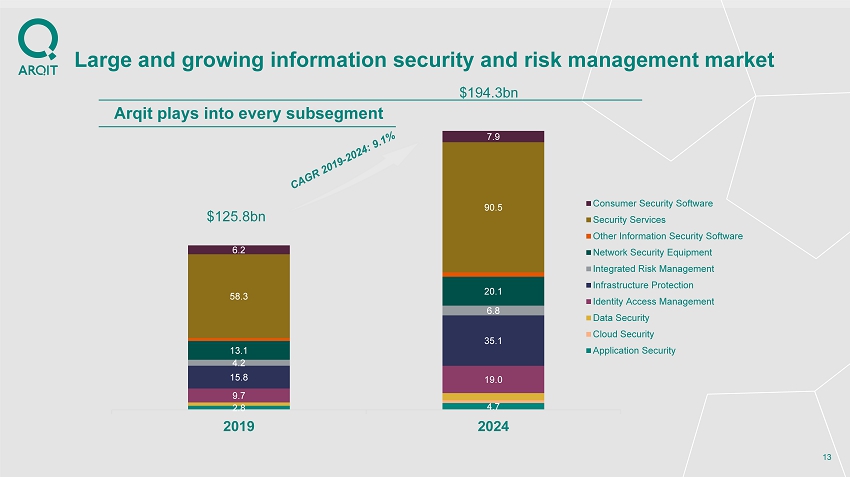

Large and growing information security and risk management market 13 Arqit plays into every subsegment $125.8bn $194.3bn 2.8 4.7 9.7 19.0 15.8 35.1 4.2 6.8 13.1 20.1 58.3 90.5 6.2 7.9 2019 2024 Consumer Security Software Security Services Other Information Security Software Network Security Equipment Integrated Risk Management Infrastructure Protection Identity Access Management Data Security Cloud Security Application Security

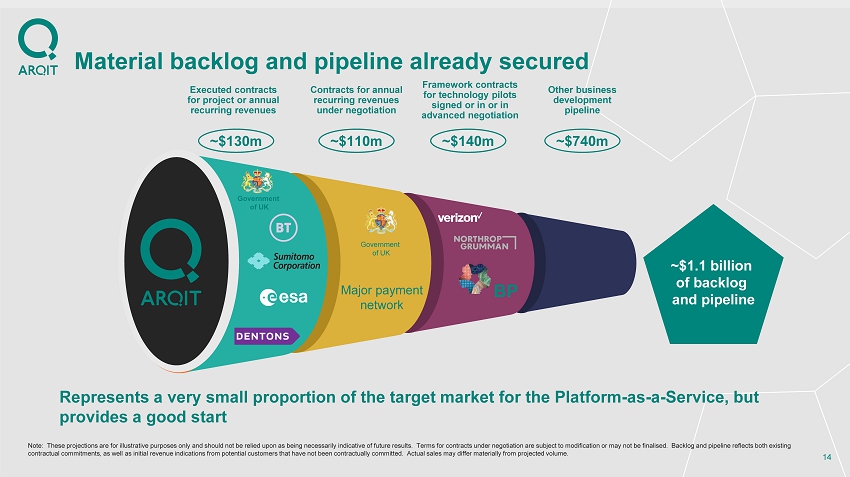

Material backlog and pipeline already secured 14 Government of UK Government of UK ~$1.1 billion of backlog and pipeline ~$130m ~$110m ~$140m ~$740m Executed contracts for project or annual recurring revenues Contracts for annual recurring revenues under negotiation Framework contracts for technology pilots signed or in or in advanced negotiation Other business development pipeline Note: These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of fut ure results. Terms for contracts under negotiation are subject to modification or may not be finalised. Backlog and pipeline r eflects both existing contractual commitments, as well as initial revenue indications from potential customers that have not been contractually com mit ted. Actual sales may differ materially from projected volume. BP Represents a very small proportion of the target market for the Platform - as - a - Service, but provides a good start Major payment network

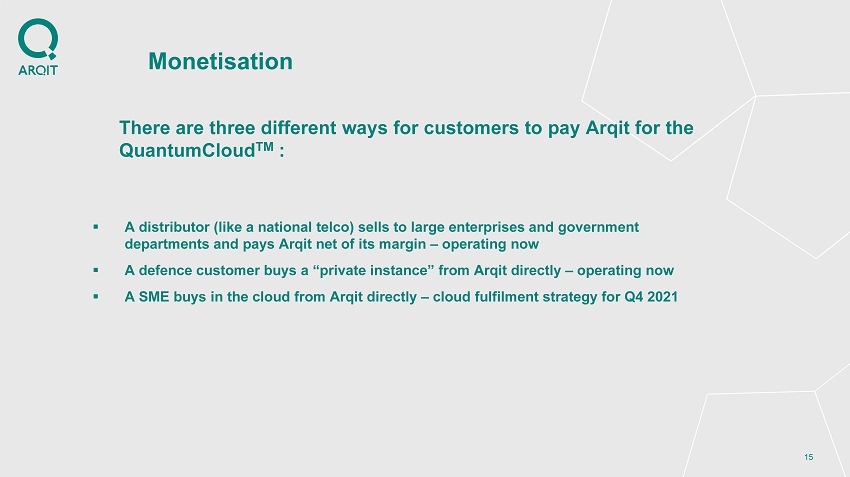

15 Monetisation ▪ There are three different ways for customers to pay Arqit for the QuantumCloud TM : ▪ A distributor (like a national telco) sells to large enterprises and government departments and pays Arqit net of its margin – operating now ▪ A defence customer buys a “private instance” from Arqit directly – operating now ▪ A SME buys in the cloud from Arqit directly – cloud fulfilment strategy for Q4 2021

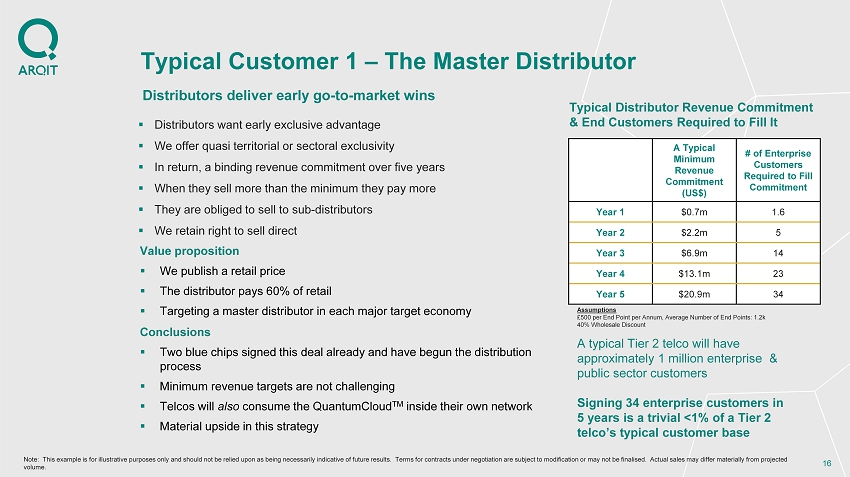

Distributors deliver early go - to - market wins 16 Typical Customer 1 – The Master Distributor ▪ Distributors want early exclusive advantage ▪ We offer quasi territorial or sectoral exclusivity ▪ In return, a binding revenue commitment over five years ▪ When they sell more than the minimum they pay more ▪ They are obliged to sell to sub - distributors ▪ We retain right to sell direct Value proposition ▪ We publish a retail price ▪ The distributor pays 60% of retail ▪ Targeting a master distributor in each major target economy A Typical Minimum Revenue Commitment (US$) # of Enterprise Customers Required to Fill Commitment Year 1 $0.7m 1.6 Year 2 $2.2m 5 Year 3 $6.9m 14 Year 4 $13.1m 23 Year 5 $20.9m 34 Assumptions £500 per End Point per Annum, Average Number of End Points: 1.2k 40% Wholesale Discount A typical Tier 2 telco will have approximately 1 million enterprise & public sector customers Signing 34 enterprise customers in 5 years is a trivial <1% of a Tier 2 telco’s typical customer base Conclusions ▪ Two blue chips signed this deal already and have begun the distribution process ▪ Minimum revenue targets are not challenging ▪ Telcos will also consume the QuantumCloud TM inside their own network ▪ Material upside in this strategy Typical Distributor Revenue Commitment & End Customers Required to Fill It Note: This example is for illustrative purposes only and should not be relied upon as being necessarily indicative of future re sults. Terms for contracts under negotiation are subject to modification or may not be finalised. Actual sales may differ mate rially from projected volume.

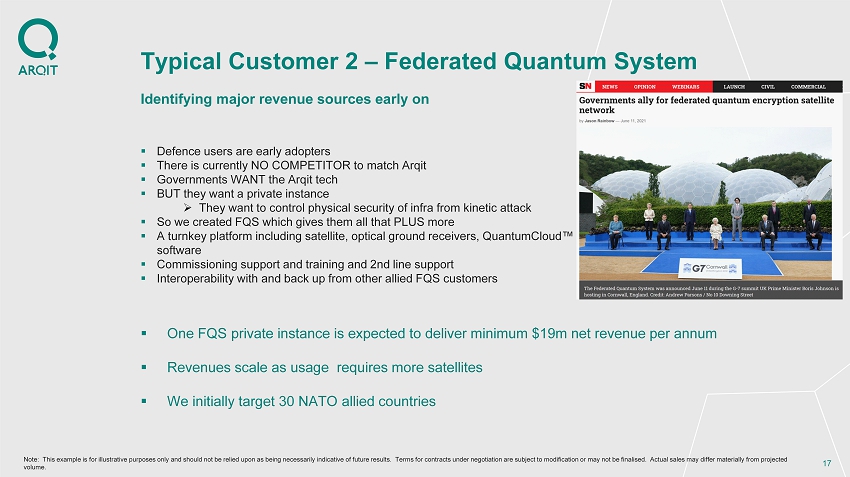

Identifying major revenue sources early on 17 Typical Customer 2 – Federated Quantum System ▪ Defence users are early adopters ▪ There is currently NO COMPETITOR to match Arqit ▪ Governments WANT the Arqit tech ▪ BUT they want a private instance » They want to control physical security of infra from kinetic attack ▪ So we created FQS which gives them all that PLUS more ▪ A turnkey platform including satellite, optical ground receivers, QuantumCloud software ▪ Commissioning support and training and 2nd line support ▪ Interoperability with and back up from other allied FQS customers ▪ One FQS private instance is expected to deliver minimum $19m net revenue per annum ▪ Revenues scale as usage requires more satellites ▪ We initially target 30 NATO allied countries Note: This example is for illustrative purposes only and should not be relied upon as being necessarily indicative of future re sults. Terms for contracts under negotiation are subject to modification or may not be finalised. Actual sales may differ mate rially from projected volume.

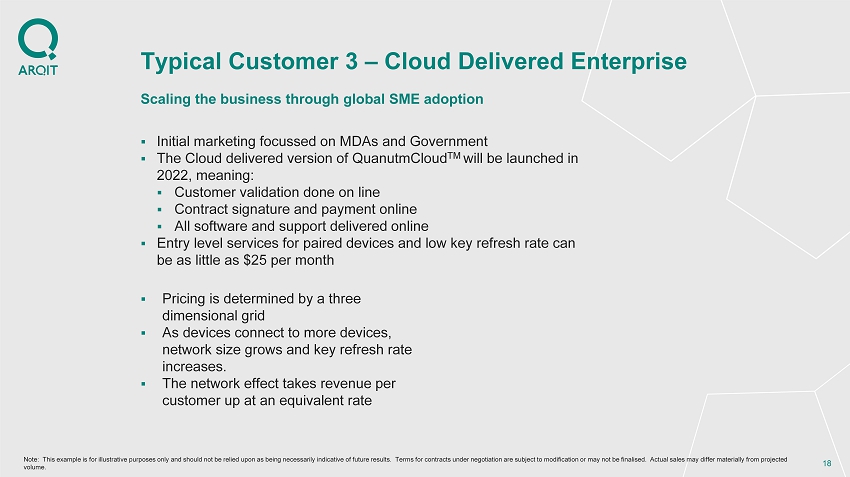

Scaling the business through global SME adoption 18 Typical Customer 3 – Cloud Delivered Enterprise ▪ Initial marketing focussed on MDAs and Government ▪ The Cloud delivered version of QuanutmCloud TM will be launched in 2022, meaning: ▪ Customer validation done on line ▪ Contract signature and payment online ▪ All software and support delivered online ▪ Entry level services for paired devices and low key refresh rate can be as little as $25 per month Note: This example is for illustrative purposes only and should not be relied upon as being necessarily indicative of future re sults. Terms for contracts under negotiation are subject to modification or may not be finalised. Actual sales may differ mate rially from projected volume. ▪ Pricing is determined by a three dimensional grid ▪ As devices connect to more devices, network size grows and key refresh rate increases. ▪ The network effect takes revenue per customer up at an equivalent rate

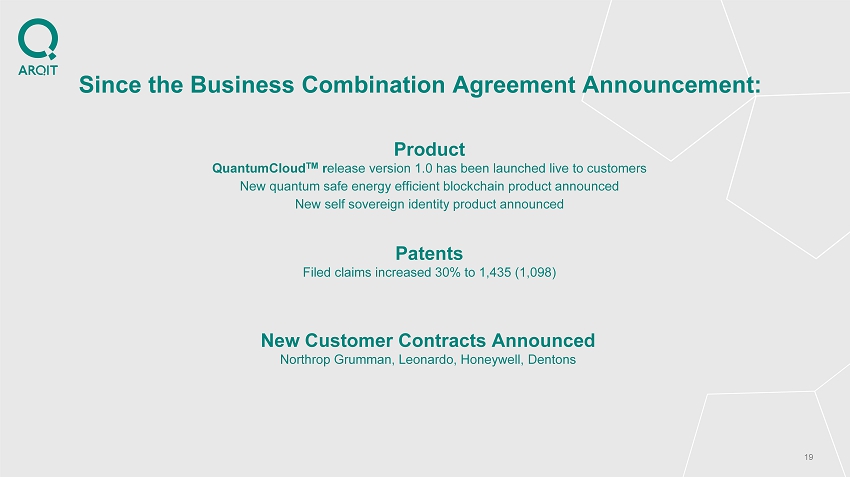

19 Since the Business Combination Agreement Announcement: Patents Filed claims increased 30% to 1,435 (1,098) Product QuantumCloud TM r elease version 1.0 has been launched live to customers New quantum safe energy efficient blockchain product announced New self sovereign identity product announced New Customer Contracts Announced Northrop Grumman, Leonardo, Honeywell, Dentons

Financial and Transaction Overview

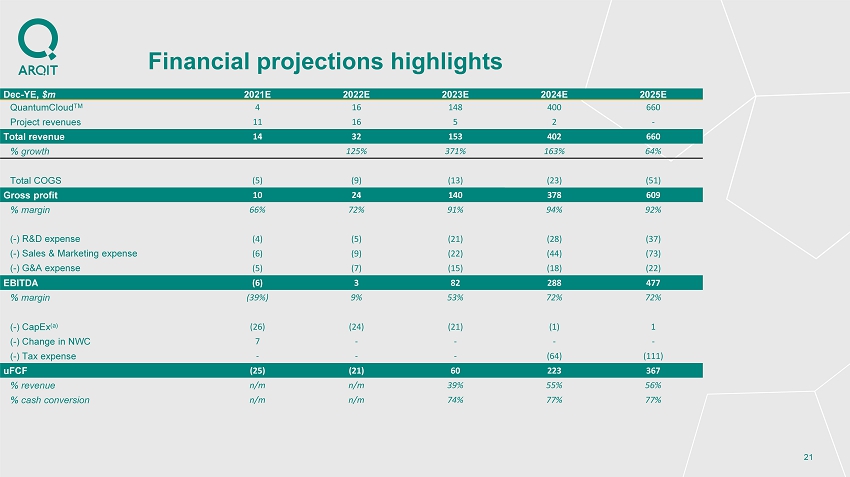

21 Financial projections highlights Dec - YE, $ m 2021E 2022E 2023E 2024E 2025E Quantum Cloud TM 4 16 148 400 660 Project revenues 11 16 5 2 - Total r evenue 14 32 153 402 660 % growth 125% 371% 163% 64% Total COGS (5) (9) (13) (23) (51) Gross profit 10 24 140 378 609 % margin 66% 72% 91% 94% 92% ( - ) R&D expense (4) (5) (21) (28) (37) ( - ) Sales & Marketing expense (6) (9) (22) (44) (73) ( - ) G&A expense (5) (7) (15) (18) (22) EBITDA (6) 3 82 288 477 % margin (39%) 9% 53% 72% 72% ( - ) CapEx (a) (26) (24) (21) (1) 1 ( - ) Change in NWC 7 - - - - ( - ) Tax expense - - - (64) (111) uFCF (25) (21) 60 223 367 % revenue n/m n/m 39% 55% 56% % cash conversion n/m n/m 74% 77% 77%

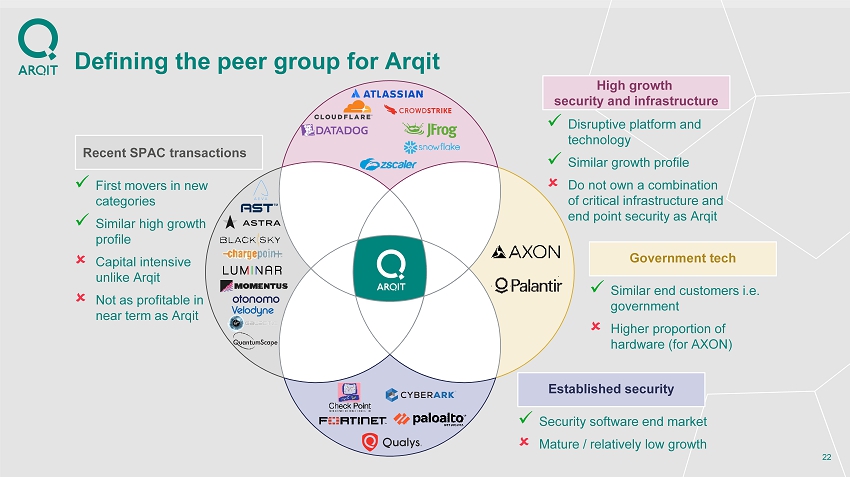

Defining the peer group for Arqit 22 x First movers in new categories x Similar high growth profile Capital intensive unlike Arqit Not as profitable in near term as Arqit Recent SPAC transactions Established security x Security software end market Mature / relatively low growth Government tech x Similar end customers i.e. government Higher proportion of hardware (for AXON) High growth security and infrastructure x Disruptive platform and technology x Similar growth profile Do not own a combination of critical infrastructure and end point security as Arqit

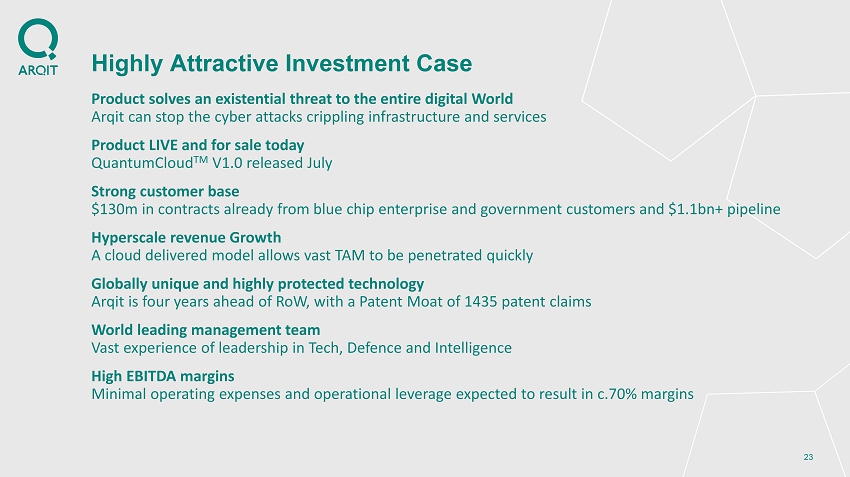

23 Highly Attractive Investment Case Product solves an existential threat to the entire digital World Arqit can stop the cyber attacks crippling infrastructure and services Product LIVE and for sale today QuantumCloud TM V1.0 released July Strong customer base $130m in contracts already from blue chip enterprise and government customers and $1.1bn+ pipeline Hyperscale revenue Growth A cloud delivered model allows vast TAM to be penetrated quickly Globally unique and highly protected technology Arqit is four years ahead of RoW, with a Patent Moat of 1435 patent claims World leading management team Vast experience of leadership in Tech, Defence and Intelligence High EBITDA margins Minimal operating expenses and operational leverage expected to result in c.70% margins

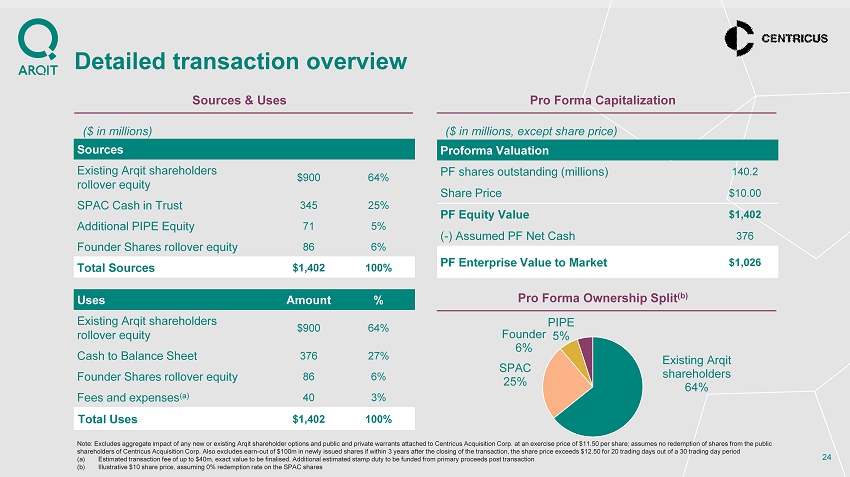

Detailed transaction overview 24 Sources & Uses Pro Forma Capitalization ($ in millions) Sources Amount % Existing Arqit shareholders rollover equity $900 64% SPAC Cash in Trust 345 25% Additional PIPE Equity 71 5% Founder Shares rollover equity 86 6% Total Sources $1,402 100% Uses Amount % Existing Arqit shareholders rollover equity $900 64% Cash to Balance Sheet 376 27% Founder Shares rollover equity 86 6% Fees and expenses (a) 40 3% Total Uses $1,402 100% Proforma Valuation Amount PF shares outstanding (millions) 140.2 Share Price $10.00 PF Equity Value $1,402 ( - ) Assumed PF Net Cash 376 PF Enterprise Value to Market $1,026 Pro Forma Ownership Split (b) Note: Excludes aggregate impact of any new or existing Arqit shareholder options and public and private warrants attached to Cen tricus Acquisition Corp. at an exercise price of $11.50 per share; assumes no redemption of shares from the public shareholders of Centricus Acquisition Corp. Also excludes earn - out of $100m in newly issued shares if within 3 years after the c losing of the transaction, the share price exceeds $12.50 for 20 trading days out of a 30 trading day period (a) Estimated transaction fee of up to $40m, exact value to be finalised. Additional estimated stamp duty to be funded from prima ry proceeds post transaction (b) Illustrative $10 share price, assuming 0% redemption rate on the SPAC shares ($ in millions, except share price) Existing Arqit shareholders 64% SPAC 25% Founder 6% PIPE 5%

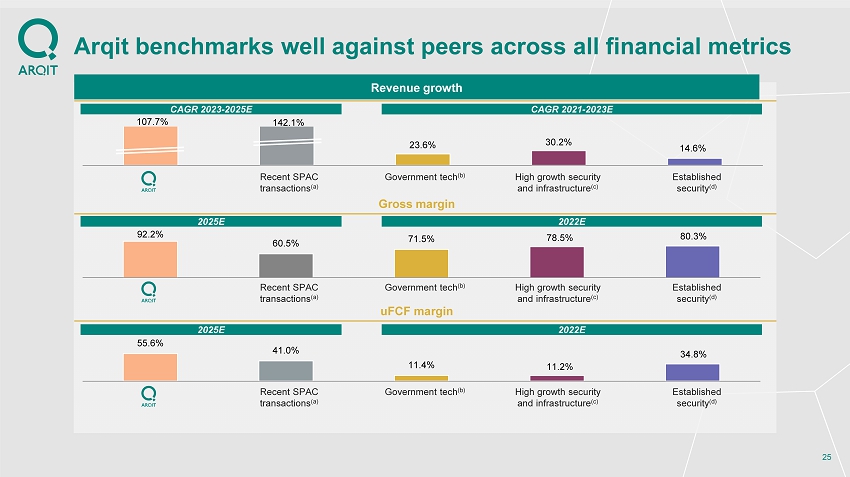

107.7% 142.1% 23.6% 30.2% 14.6% Arqit benchmarks well against peers across all financial metrics 25 Revenue growth Gross margin uFCF margin High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) CAGR 2023 - 2025E CAGR 2021 - 2023E 2025E 2022E 2025E 2022E 92.2% 60.5% 71.5% 78.5% 80.3% 55.6% 41.0% 11.4% 11.2% 34.8%

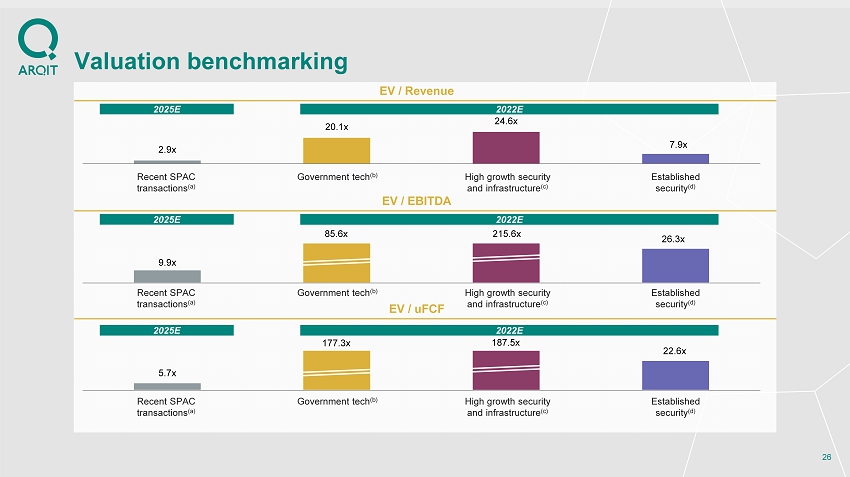

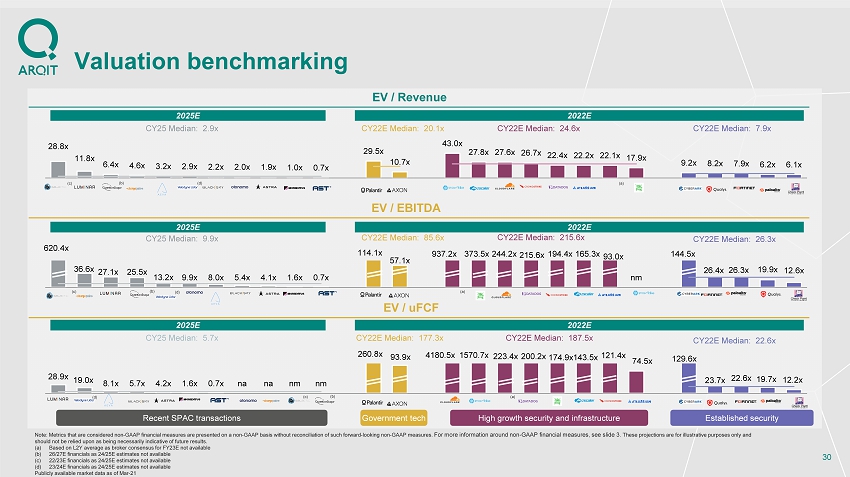

5.7x 177.3x 187.5x 22.6x 9.9x 85.6x 215.6x 26.3x Valuation benchmarking 26 EV / Revenue EV / EBITDA EV / uFCF High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) 2025E 2022E 2025E 2022E 2025E 2022E 2.9x 20.1x 24.6x 7.9x

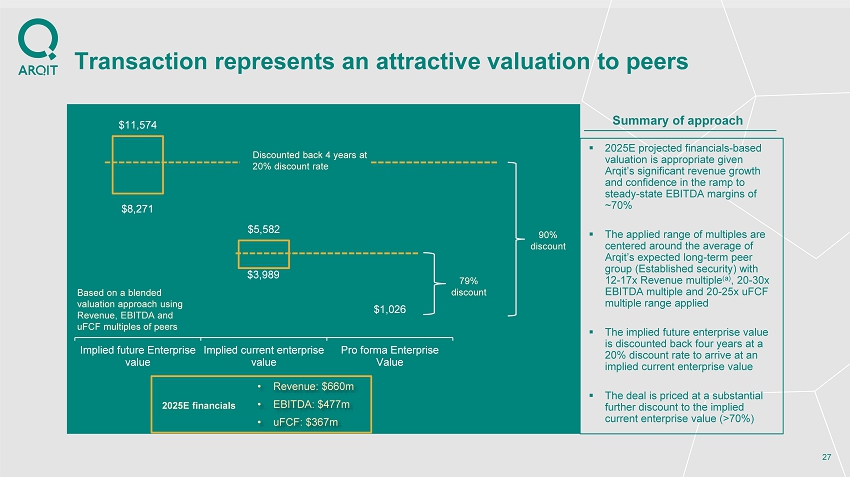

$8,271 $3,989 $1,026 $11,574 $5,582 Implied future Enterprise value Implied current enterprise value Pro forma Enterprise Value Transaction represents an attractive valuation to peers 27 ▪ 2025E projected financials - based valuation is appropriate given Arqit’s significant revenue growth and confidence in the ramp to steady - state EBITDA margins of ~70% ▪ The applied range of multiples are centered around the average of Arqit’s expected long - term peer group (Established security) with 12 - 17x Revenue multiple (a) , 20 - 30x EBITDA multiple and 20 - 25x uFCF multiple range applied ▪ The implied future enterprise value is discounted back four years at a 20% discount rate to arrive at an implied current enterprise value ▪ The deal is priced at a substantial further discount to the implied current enterprise value (>70%) Based on a blended valuation approach using Revenue, EBITDA and uFCF multiples of peers Discounted back 4 years at 20% discount rate 79% discount 90% discount • Revenue: $660m • EBITDA: $477m • uFCF: $367m 2025E financials Summary of approach

Additional Materials Benchmarking

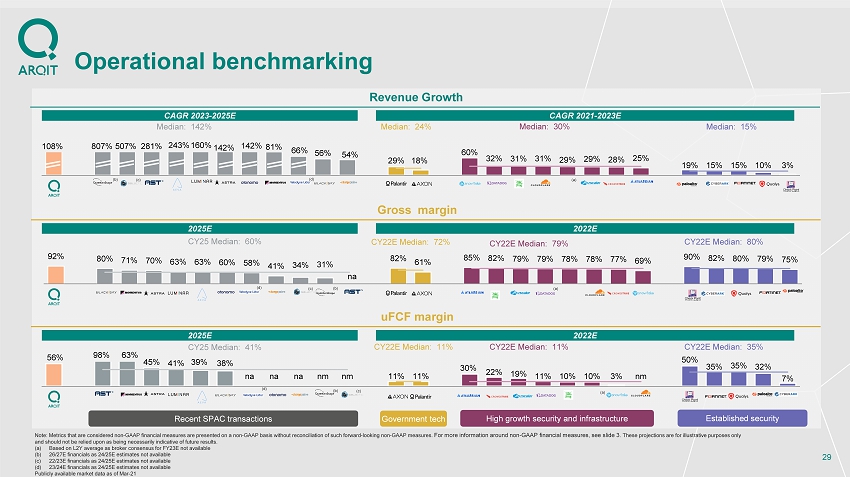

92% 80% 71% 70% 63% 63% 60% 58% 41% 34% 31% na 82% 61% 85% 82% 79% 79% 78% 78% 77% 69% 90% 82% 80% 79% 75% CY22E Median: 79 % CY25 Median: 60% CY22E Median: 80% CY22E Median: 72% 56% 98% 63% 45% 41% 39% 38% na na na nm nm 11% 11% 30% 22% 19% 11% 10% 10% 3% nm 50% 35% 35% 32% 7% CY22E Median: 11% CY25 Median: 41% CY22E Median: 35% CY22E Median: 11% 108% 807% 507% 281% 243% 160% 142% 142% 81% 66% 56% 54% 29% 18% 60% 32% 31% 31% 29% 29% 28% 25% 19% 15% 15% 10% 3% Median: 30% Median: 15 % Median: 24 % Median: 142 % Operational benchmarking 29 CAGR 2023 - 2025E CAGR 2021 - 2023E High growth security and infrastructure Established security Recent SPAC transactions Government tech Revenue Growth Gross margin uFCF margin 2025E 2022E 2025E 2022E (b) (c) (a) (b) (c) (a) Note: Metrics that are considered non - GAAP financial measures are presented on a non - GAAP basis without reconciliation of such f orward - looking non - GAAP measures. For more information around non - GAAP financial measures, see slide 3. These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. (a) Based on L2Y average as broker consensus for FY23E not available (b) 26/27E financials as 24/25E estimates not available (c) 22/23E financials as 24/25E estimates not available (d) 23/24E financials as 24/25E estimates not available Publicly available market data as of Mar - 21 (b) (c) (a) (d) (d) (d)

620.4x 36.6x 27.1x 25.5x 13.2x 9.9x 8.0x 5.4x 4.1x 1.6x 0.7x 114.1x 57.1x 937.2x 373.5x 244.2x 215.6x 194.4x 165.3x 93.0x nm 144.5x 26.4x 26.3x 19.9x 12.6x CY25 Median: 9.9x CY22E Median: 26.3x CY22E Median: 85.6x CY22E Median: 215.6x 28.9x 19.0x 8.1x 5.7x 4.2x 1.6x 0.7x na na nm nm 260.8x 93.9x 4180.5x 1570.7x 223.4x 200.2x 174.9x 143.5x 121.4x 74.5x 129.6x 23.7x 22.6x 19.7x 12.2x CY22E Median: 22.6x CY25 Median: 5.7x CY22E Median: 177.3x CY22E Median: 187.5x 28.8x 11.8x 6.4x 4.6x 3.2x 2.9x 2.2x 2.0x 1.9x 1.0x 0.7x 29.5x 10.7x 43.0x 27.8x 27.6x 26.7x 22.4x 22.2x 22.1x 17.9x 9.2x 8.2x 7.9x 6.2x 6.1x CY25 Median: 2.9x CY22E Median: 24.6x CY22E Median: 7.9x CY22E Median: 20.1x Valuation benchmarking 30 EV / Revenue EV / uFCF EV / EBITDA High growth security and infrastructure Established security Recent SPAC transactions Government tech 2025E 2022E 2025E 2022E 2025E 2022E (b) (c) (a) (b) (c) (a) (b) (c) (a) Note: Metrics that are considered non - GAAP financial measures are presented on a non - GAAP basis without reconciliation of such f orward - looking non - GAAP measures. For more information around non - GAAP financial measures, see slide 3. These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. (a) Based on L2Y average as broker consensus for FY23E not available (b) 26/27E financials as 24/25E estimates not available (c) 22/23E financials as 24/25E estimates not available (d) 23/24E financials as 24/25E estimates not available Publicly available market data as of Mar - 21 (d) (d) (d)

This transcript was exported on Aug 19, 2021 - view latest version here.

John Yi (00:00:17):

(Silence)

John Yi (00:00:25):

All right. Hello everyone. Thank you very much for joining us today for the Arqit and Centricus Public Investor and Analyst day. My name is John Yi and I'm one of the IR advisors for Arqit. With me today are Arqit CEO, David Williams, Arqit CFO, Nick Pointon and Centricus CEO, Garth Richie. The format today will be a presentation by David Williams, followed by a Q and A session. To submit a question, please use the chat function on your Zoom platform, and we'll do our best to answer your questions following the conclusion of the presentation. With that said, I'll now turn it over to Garth, CEO of Centricus. Garth.

Garth Richie (00:01:02):

Thanks, John. Um, good day, everybody as advertised, I'm Garth Richie and Chief Executives of Centricus Acquisition Corp. On behalf of our board and our chairman Manfredi Lefebvre, we are delighted to bring, um, the business combination, which we are presenting to you today, which is Arqit. Um, the founder and CEO David will talk to you in a second. I would just say to you that we are, um, have $345 million in trust. Um, we have already had our record date and we expect the AGM to be the last day of the month, the 31st of August. Um, we are currently trading in the market. Uh, we have reasonably good liquidity, we're trading just in and around the bond flow or the trust value.

Garth Richie (00:01:47):

We are incredibly excited about this company. We're committed to the company. We've done a serious amount of due diligence, both on the technology, on the cu- customer contracts and on the competence of management. Um, and we feel that we have been, um, unanimous in our recommendation that, uh, to our shareholders, that they should endorse this transaction. So without further ado, over to the CEO and founder, David Williams.

David Williams (00:02:13):

Thank you, Garth. And hello everyone. Thank you so much for joining us today. Arqit's mission is to use its world-leading quantum encryption platform to keep safe the data of our governments, enterprises and citizens. In the five years of invention since the company was created, we've built a tech stack, which has some very complicated uh, quantum technology in the background. Uh, but which creates an incredibly simple product, just a lightweight software agent, which is downloadable onto any form of end point device or cloud machine. And it allows that device to create encryption keys, which are three important things that's computationally secure, which means it can't be broken by any form of future computer.

David Williams (00:03:06):

Zero trust, which means that no other device ever knew the key, and one time, which means the key never existed until the moment it's created. It's used once and then thrown away. We can create those keys in infinite numbers and infinite group sizes. Now the combination of computationally secure zero trust and one time, that Trinity of features is the holy grail of cybersecurity. There has never been another company that's able to create such encryption keys and to do it at such scale product. The product is live with customers today. We're already taking the software to market. We're doing it at pace and at the consummation of this business combination agreement with Garth and his team, we expect to be able to greatly accelerate our customer traction. Today I'm gonna talk to you a little bit about the technology. Um, I love talking about the tech, but I'm not gonna do a deep dive today. If there is anybody on the call who loves the tech and wants to know a lot more about it, we should have some time afterwards, but I'm also very happy, I and my, my team are happy to spend time with institutional investors that want to do a deep dive on tech. But today I wanna focus on the commercial traction and particularly to explain how that traction has accelerated since we announced the business combination agreement up to the point where we actually launched live service last month.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 1 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:04:38):

Thanks Nick. So, the problem statement, we all know that public key encryption was never designed to protect a hyper-connected world. The cyber-attacks that we're seeing every day now arise because the encryption that we use was invented many decades ago and it's done a great job, but it wasn't designed to do what we're all asking it to do today. Our governments appreciates that most acutely, the American government has urged us all to find new solutions. The solutions that the world has been looking for have not proven to be compelling. Nick.

David Williams (00:05:19):

So Arqit has the solution. It's to be found in a thing called a symmetric key. Um, unlike public key cryptography, there's no maths involved in symmetric keys. Uh, symmetric keys are just random numbers. And so, computers have got no ability to reverse engineer these keys. They've never been capable of distributing at scale. Mainly they've been used by our governments and banks, uh, distributed using human courier. There's never been a provably secure way to distribute these keys at scale, but because such keys have been used for decades, they're already baked into the world software networking systems. There's an algorithm called AES 256, which is universally held to be unbreakable. And that is already standardized in virtually all of the world's software systems.

David Williams (00:06:10):

So Arqit's innovation is in creating a method for distributing or creating unbreakable symmetric encryption keys at scale, once the keys are created, they just slot into the existing software system. So Arqit's solution does not request the world to make fundamental changes to its hardware and software. Nick. Um, you'll be, uh, interested perhaps to do a deeper dive into the people. I just wanted to say that Arqit was co-founded, uh, with a group of four former directors of GCHQ Britain Signals Intelligence Agency, along with a cohort of great American cryptographers from the private sector and the American defense establishment. This is without doubt in our view, the greatest team of cryptographers uh, ever assembled for any startup company. The innovation behind our product is in two areas. Firstly, we use some very complex quantum encryption systems using satellites. What they do is put an identical set of unbreakable symmetric encryption keys into every data center in the world. The ability to do that in a secure and scalable way is unique to Arqit. Once those keys are there, a brand new crypto mathematical software system invented by Arqit is able to borrow elements of those keys from the cloud and use them as ingredients in making brand new keys locally.

David Williams (00:07:56):

So these keys are never existing somewhere else. They're made locally on the devices when they're needed. Those devices can be IOT sensors, phones or F-35 fighter jets. It doesn't matter. It's the same lightware software agent, regardless of the application. And that's ultimately what makes Arqit potentially a hyper scaling business. It's a cloud delivered piece of software that is universal to every single application. Nick.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 2 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:08:29):

It helps in credentialing the technology, I think for our investors to be able to see what the leaders of customers and governments and blue chip organizations are actually saying about us in public. So whether it's ministers of the British government, chief technology officers at companies like British Telecom, Sumitomo of Japan, Honeywell, Leonardo in the UK, Northrop Grumman in America, these great companies have embraced our technology, signed contracts, bought the system and declared in public that this technology is extremely important.

David Williams (00:09:04):

In our opinion, Arqit's technology is the most important cybersecurity technology of its era, and the growing cohort of large scale government and co- and commercial organizations agree with us. that technology is protected by a very deep and wide patent modes. Um, we have over 1,400 patient claims filed. We deliberately remained very quiet about our technology for the four and a half years of invention. Uh, since the very beginning, we knew that we had solved some really fundamental problems for mankind, and we knew that if we were going to exploit that properly, we have to protect it with patent filings.

David Williams (00:09:48):

So we spent an enormous amount of time, effort and treasure on uh, making patent filings. And we believe that the very complicated family of patents that we've created will allow us to maintain our lead to market. All of our intelligence tells us that our lead to market currently is four years. We believe that our technology is at least four years ahead of any other organization in the world. And we think that the patent moat buys us enough time to protect that advantage so that we can build our revenues to the point where it's the revenues that will protect this company. I'll move on from this slide and go to the, uh, this pipeline slide. Um, we started selling only in the middle of last year and already to the point of the business combination announcement in May, we built a backlog of potential revenues of $1.1 billion. And we did that with just two salespeople, one of which is me. The backlog, or rather the pipeline also includes a backlog of $130 million of binding revenue contracts. So these are contracts where the revenues will definitely be delivered. So we've, we've been able to generate a really quite impressive backlog of revenues with a very small amount of sales and marketing.

David Williams (00:11:15):

As you would imagine, through the process of announcing the stack and promoting it, we've come to much broader attention. And the credentialing effect of the stack I believe has accelerated our sales cycle. So when I next report this number to you in the next regulated reporting moment, you might reasonably expect those numbers to have risen.

David Williams (00:11:40):

So I want to dwell on customers. Uh, the technology is important, but this is how I generate a superior return for our investors. We focus to begin with on a cohort of customers in four broad areas. Ultimately, this is a cloud delivered product, which is available to all and every, uh, sensible, accredited customer in the world. But we focused our early efforts on these four sectors. in telecommunications, British Telecom has been a pioneer in the creation of internet technologies. It invented the hyperlink. It's been at the heart of the uh, most important innovations in the history of the internet.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 3 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:12:24):

Um, but of course, as the provider of national security telecoms networking, not only to the British, but also to be American and other governments around the world, it's a very cautious technology company, but BT has been a foundational partner for Arqit since the beginning. And earlier this year, it's signed a multi-year multi tens of millions of pounds contract to buy our technology and to take it to market. And I'm very proud that Howard Watson, its chief technology officer, has put his weight fully behind Arqit in public, through quotes that you've seen in press releases.

David Williams (00:13:01):

We're doing some great work with Verizon in the United States, who are a pioneer in thinking about quantum technologies. And we're particularly focusing on 5G, and we have an interesting developing relationship with Juniper. We believe it's important that Arqit's technology is baked into the equipment of the world's most important vendors. In fact, you'll see some other logos joining that vendor group quite soon. Defense has been very important to us. The UK government has also been a foundational customer since the beginning, but we made a very big breakthrough in Japan last year with again, a multi-year multi tens of million pound contract with Sumitomo Corporation, one of the most important defense integrators in Japan.

David Williams (00:13:47):

Sumitomo are selling our technology not only to the Japanese government, but now also into the telecoms market. It was very important for us to bring an American defense systems integrator into the customer group very early and Northrop Grumman, uh, I'm delighted to say, did embrace the technology very early and are becoming a very interesting partner. You will see more development from us, uh, in the, uh, area of securing the future battle space. Um, we've found that our technology is regarded as of fundamental importance to a concept, which I'd like you all to be aware of called Joint All-Domain Command and Control.

David Williams (00:14:31):

This phrase describes how the American military thinks of its data challenges of the future. How does every single piece of equipment get to receive the right information at the right time with the right level of classification? How do we change those information sharing groups? How do we manage information sharing between companies, and divisions, and branches and nations? This is an incredibly complex multidimensional task, and of fundamental importance to our ability to have machine to machine communications on the future battle space.

David Williams (00:15:12):

I think it's important to note, uh, that general Wilson, um, who honored us with his presence on our board, formally the four-star vice chief of the United States Air Force, observed in public, that Arqit has solved the cybersecurity layer problem within Joint All-Domain Command and Control. You should not underestimate the importance of that statement. We believe it will translate into very significant projects in the near future. And we are working now with a very important consortium of companies towards the ambition of seeing Arqit's technology integrated into the future of secure communications for our military customers. Please keep a close eye out for further announcements on that subject.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 4 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:15:57):

In financial services, uh, we're already working with at least one major payment network and with Dentons, which are the largest law firm in the world. We're building a system which we think is the future of identity. People and machines have great difficulty proving their identity. proving your identity whilst protecting your privacy is one of the greatest problems of our era. How do I stop my data from being leaked in a data breach? How do I stop unfavorable actors from accessing my private information when they have no right to do so? Balancing these two things is one of the most important aspects of what Arqit has to bring to the world.

David Williams (00:16:39):

Dentons as the largest law firm in the world has helped us to craft a system that does just that. Uh, you'll see that product launching to market in Q4. And we believe it will provide the underpinning, not only of secure identity management systems in areas like law, but also in financial services and ultimately in government and other, other important areas like blockchain. We had important growing relationships with organizations that are developing the future of automation, whether it's in smart cars uh, or smart cities. And that, and our work in identity has also led us into blockchain.

David Williams (00:17:20):

Uh, Arqit's co-founders, many of them, have been involved since the very, very beginning of blockchain technology. Well before, uh, the Nakamoto paper on Bitcoin. And we do have fundamental belief that blockchain technology has an important role to play in the world in a number of areas. Most obviously, in those areas where multiple parties need to keep the same records, but also in financial payments. We observed that central banks have increasingly been making statements about the importance of what are known as central bank digital currencies. These are governments simply embracing blockchain technology for the future of money, and we believe that's going to happen, but there is one fundamental problem and that's the blockchain technology uses public key cryptography to sign its transactions.

David Williams (00:18:09):

Those encryption schemes are fundamentally quantum broken. There can be no doubt that they are compromised and that, that is almost certainly happening in this decade. So it's highly unwise for anyone to contemplate putting significant value or importance onto a blockchain system, if we know that that compromise is universal and eminent. The prospect of using upgraded public key cryptography, what are known as post quantum algorithms is also in our opinion preposterous. These algorithms achieve a slightly higher level of security, simply by becoming much, much larger.

David Williams (00:18:49):

Like many software systems, blockchain most acutely is very sensitive to things like latency and block size. And we put some research out recently, which demonstrates that such algorithms are 1,400 times the processing cycles of Arqit's technology. Therefore, we do have a fundamentally important role to play in the future of blockchain. And we intend to do that not only with central bank digital currencies, but also we believe that a number of commercial organizations are likely to issue their own versions of such currencies and Arqit intends to play an important role in building such systems. Thank you, Nick.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 5 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:19:35):

So I want to dive down into the detail now of explaining to you how the traction that we have with customers turns into cash. Um, our product is the same wherever we go. Ultimately, it's just 200 lines of code that sits on any device and with infinite group sizes and infinite key refresh rates, creates keys that are zero trust and unbreakable. The product is the same wherever we go.

PART 1 OF 4 ENDS [00:20:04]

David Williams (00:20:03):

There are, however, three different ways for a customer to buy it. Firstly, we have channel partners, sometimes called distributors. They take the product from Arqit, they guarantee to pay for it, and they, they then sell it to their enterprise or government customers.

David Williams (00:20:21):

Secondly, in national security in defense, our customers there, for various important reasons, want to buy private instance. This is in fact how government organizations and defense buy cloud services. So a private instance sold from Arqit directly to a defense department is a very important method of selling. Finally, the way we believe that ultimately Arqit scales its business to the highest level is by making its product available in the cloud. So I'll now give you some more worked examples of each of these three.

David Williams (00:20:57):

Channel partners are obviously to us very keen, not only to use the product, but to secure some element of exclusivity. I'm still surprised that after some 30 years of being a salesman, I've learned that Arqit customers don't say no to us. When we engage in a deep dive with the customer, the customer progresses to a contract of some form. It's obvious to us that customers recognize that this technology is wildly important. And we are seeing that channel partners want to lock in a degree of exclusivity.

David Williams (00:21:35):

We're okay with that as long as it doesn't retard the growth of the business, because we think that it's important to show our stakeholders that we've got long-term revenues baked into what the company does. We think that gives all of our stakeholders, whether it's our employees, our customers or our shareholders, confidence in the future of the company. So with channel partners, we do enter into deals where they typically take limited exclusivity. It could be in a territory or it could be a sector. In return for that, they guarantee to pay us a minimum amount of revenue.

David Williams (00:22:11):

So a channel partner in an average sized country might typically pay us a million dollars a year in the first year rising to $20 million in the fifth year. That gives us a guaranteed backbone of revenue ramping up over a five-year period. That company will now look to take the product to market and sell it in as high a volume as possible to its enterprise customers.

David Williams (00:22:39):

If we look at a typical telecommunications company in an average sized country, we'll see that such a telco might have one million enterprise customers. And when we look at the average deal size for an average enterprise customer, we see that that channel partner only in fact needs to sign 34 enterprise customers in order to fully satisfy his minimum revenue guarantee in year five.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 6 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:23:08):

So if a telco has a million customers and he only needs to sign 34 to hit that minimum revenue guarantee, we feel that we can have very high confidence that this commercial strategy is likely to exceed our own hopes and targets. You can do the math yourself. We're targeting initially partners in 30 NATO allied countries. If we're successful in doing that, we would bake in over $600 million of annual revenue by year five. As we'll show on subsequent slides, the entire revenue target for the company in year five is just $660 million.

David Williams (00:23:52):

So this commercial strategy with distribution partners or channel partners is very important in baking in revenues that we think can take us to that target. But that's not the only way that we can do it. On the next slide, we talk about the private instance. We learned from our defense customers that whilst they understand that the Arqit technology is everything that we say it is, that it can create compelling strategic advantage for them and that, most importantly, Arqit itself can never know the keys that it creates, there is one problem that Arqit can't solve, and that's that a defense department customer wants to have physical control of its security infrastructure, because in a time of war, the possibility of a kinetic attack has to be defended. And Arqit can't do that.

David Williams (00:24:45):

So for that reason, our defense customers want an end-to-end private instance of our technology, and we created a version of that tech that we currently call FQS, which stands for the Federated Quantum System. Under this commercial methodology, we deliver to the defense department customer an end-to-end turnkey version of our technology, which includes a satellite launched in orbit, optical ground receivers, QuantumCloud software in the data centers, end point software for all of their devices, ongoing commissioning support, training and software upgrades.

David Williams (00:25:23):

Critically, that technology also is interoperable with the FQS systems of other allied countries. It's important that an, an American fighter jet can talk to a British fighter jet. The Brits and the Americans can have their own FQS systems, but they can also be rendered interoperable. This is an incredibly important feature of delivering on the future promise of the joint all demand command and control strategy. And we believe that Arqit alone is the only company in the world that can deliver this.

David Williams (00:25:55):

Typically, one FQS private instance will generate total revenues of about $25 million per annum, net of basic hardware costs about $90 million of net revenue per annum. So again, if we imagine success in selling just one private instance to each of our 30 target NATO allied countries, that would deliver revenues well in excess of our $660 million a year five targets.

David Williams (00:26:22):

We've already announced at the G7 that not only has the UK signed the first contract to pursue an FQS project but six other countries, uh, have now joined with them. And I have high confidence that you will see other countries joining that FQS project during the course of the next few months. We are very confident about the progress that we're making, particularly in the United States of America.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 7 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:26:52):

On the next slide, we explain how the cloud delivered version of our product works. Ultimately, we want any company of any size in any accredited country anywhere in the world to simply buy, contract, download, pay for, use the software in the cloud. The scale of, of use is very broad, but we have decided that the entry level for this services is as little as $25 a month and it rises to tens of millions of dollars a month.

David Williams (00:27:26):

The way, the way we bridge that gap is by pricing in a three- dimensional grid. So the three elements that determine the revenue from a customer ... Number one, how many ... to protect. Secondly, what's the key refresh rate? How often do our customers want to refresh their keys? Thirdly, what's the group size? How many devices which to communicate together? When we factor in those three elements, we get a total number of keys that the customer will use and be billed for. And that's ultimately how we determine the revenue per customer, but also we start with small volumes of keys. And then we encourage customers to, to increase their group sizes and to increase the key refresh rates. And that's how customers transition from smaller revenues to larger revenues.

David Williams (00:28:37):

This is how ultimately we think the Arqit business can grow to very high scale. I think I've shown you that with our channel partnership strategy and with our government direct strategy, we expect to be able to show you very solid underpinning for that year five revenue forecast. And we expect to deliver confidence to the market that we can achieve that in the coming quarters. But when the cloud delivered version of this service is launched and begins to grow, that's when I think you can see Arqit's value, uh, really appreciate very strongly ... Nick.

David Williams (00:29:22):

So we've made a lot of progress since we announced the business combination agreement with Centricus. We told you back in May that we expected to launch the QuantumCloud software live by the end of December. We tested it in the second quarter, and we actually launched it live in July. So we beat our own target by two quarters. And release version one has now, or, uh, is in the process of being shipped to the first 20 customers who are in the process of developing, testing and integrating it into their own systems.

David Williams (00:29:56):

We've actually issued our first live service invoice, uh, to customers. And so we are confident they're generating, uh, the anticipated levels of revenue in Q4. As I've said, we continue to, uh, file for new patents, uh, and we took it up by 30% during the period. We announced a cohort of new customer contracts, and you should expect to see more announcements from Arqit in the coming weeks. So how does all this turn into the cash that you need to see to generate a handsome return on your investments? Well QuantumCloud is the perfect example of an infinitely scalable business model. With just 200 lines of code, it works on any device, a tiny device or a large device. There is no device that QuantumCloud does not work on. We can sell this in theory to all and any customer in the world. We choose to limit ourselves at the moment to NATO allied countries, but that might change in future.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 8 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:31:05):

The revenues that we've predicted are, in my opinion, highly cautious by reference to the target portion of our own addressable market. And we've shown you that we can achieve those year five numbers even if we were to undershoot our own expectations quite dramatically. But at just that level of revenue, the profit margins are extremely high with gross margins of over 90%. The expenses are, uh, quite scalable. Uh, the invention process, uh, of the last five years has delivered a product which we believe is near perfect. But of course, we will want to find new applications for our keys and always be looking for new sources of growth.

David Williams (00:31:52):

So when we talk about R&D, we're not really talking about reinventing our technology. We're talking about developing, um, added value applications that can take us up the value curve and generate perhaps higher revenues or new revenues through things like blockchain, for example.

David Williams (00:32:10):

Our sales and marketing expense will ramp up in line with the size of the customer base. Uh, but the G&A costs are not expected to change very dramatically. So I believe that these forecasts are prudent, cautious and achievable. I think we've demonstrated with $130 million of committed and signed contracts from blue chip companies that this is not one of those hidden hope companies that is dangling the hope of, uh, great profits in future. We have a live product in the market today being embraced and welcomed publicly by some of the most important tech companies and governments in the world. The revenues are ramping up, and I think these forecasts should give you reason for cautious optimism.

David Williams (00:32:59):

We have an interesting view of competition. There are companies that provide excellent services with on-premises, uh, end point technology today and there are companies that do some really interesting things in cybersecurity and the cloud. But everyone's technology has to be baselined on strong encryption. And as I showed you earlier, public key cryptography is fatally compromised. And the solutions that the world has been working on are, by reference to the direct quotes of the American Government, "Not going to be universally viable in a short period of time."

David Williams (00:33:34):

So we have the ultimate problem statement. Everyone wants a new solution, and Arqit uniquely has it. So we don't believe that we are deeply competitive with any other or any significant cohort of cybersecurity companies. We believe that the companies that provide rich value added services up at the top, uh, portion of the Venn diagram are great target partners for us. We believe that we can help the companies that have made their money from on-premise solutions to migrate to a new form of cloud cybersecurity.

David Williams (00:34:08):

So we deliberately choose to take a non-confrontational approach to competition. We believe that any cybersecurity company in the world is a company that we want to consider working with and partnering with. We believe that we can make any company's products and service better. And we want to be seen as a good and strong corporate citizen in helping the entire cybersecurity world to move on and inject new levels of security into what everything that they currently do and everything that could be improved to become in the future. So for that reason, you will see initiatives from us in the coming quarters about elements of our technology, which may become in future open-source but certainly standardized.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 9 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

David Williams (00:34:54):

Thank you, Nick ... So now I'll ask Garth to explain how we came up with a transaction rationale.

Garth Richie (00:35:07):

Yeah, so, um, let me just talk a bit about, uh, valuation. But before, um, I talk about valuation, I just want to, uh, reassure, uh, you, what we as, as, um, Centricus brought, uh, for you as, as investors or potential investors is, uh, we did a significant due diligence on, uh, the technology. We employed experts, um, and we interrogated, uh, some of the early investors, um, who had also interrogated the technology like the UK Space Agency and Innovation UK and a number of other people that had backed this company, um, at an early stage.

Garth Richie (00:35:48):

We then also took it upon ourselves, um, to have a look at the contract, um, and talk to the customers. Uh, we spent significant time and diligence on those ensuring that they are what they say they are. And then we've taken our time obviously doing a background check on David and his management team and ensuring whether we feel that we could recommend the deal to you, um, uh, as our investors, that this was a competent management team that would be able to with, uh, withstand the scrutiny of the public markets and could actually cope with the hyper growth that we expect this company to generate.

Garth Richie (00:36:21):

Um, obviously we have unanimously recommended this to you, and therefore, they passed with flying colors. Um, furthermore, what we then have to do is we have to put together, um, a, a dissertation, for want of a better word, which we submit to the SEC. Um, as you know, I think quite justifiably, the SEC has been scrutinizing SPAC transactions and, and deals where you have reasonably young, um, growth companies with, um, future growth priced into them, uh, and had a long look at them.

Garth Richie (00:36:51):

We were, um, assured by, um, our legal counsel, um, as well as David's legal counsel that this would be a very arduous process. Um, I'm comfortable to, to let you know that actually the SEC we feel did a great job, that they had a look at our submission, which we think was incredibly robust where we described pricing, valuation. Um, we talked about the, uh, the technology, about the contracts and the, and all of the other variables that we thought were resilient. And we got through reasonably quickly with only one set of questions, which is unusual, um, according to those that, that live in the space. Um, you don't have to just take my word for it.

Garth Richie (00:37:31):

So I suppose at the end of the day, once you've decided that you've got a great company, um, and the company will withstand, uh, the scrutiny of the public markets and trade well in the public markets, um, one has to think about valuation. So in order to get a base for where you get valuation, what we did is we used public market data. Uh, we used 2025 projective financials and valuations based on, on revenue growth, EBITDA margins and a group of things just there in the market.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 10 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

Garth Richie (00:37:59):

And we took companies which we felt would be in the genre of Arqit. And then, uh, we had, we ended up coming up with a price on the slide of 11 1/2 billion was the top end, and 8.2 billion was the bottom end. And then obviously we believe that the market is discounting the probability of 2025 earnings, but this is where, uh, the market price is in today.

Garth Richie (00:38:23):

What we then did is we said, "Okay, what we would probably do is we need to discount that back for four years," and we used the discount rate of 20%. Um, we then arrived at a new, um, average, which was the difference between 5.5 billion and four billion. And what we did then is we took the middle of that and we said, "Okay, now what discount do we apply to that such that we can be sure, um, that we're gonna be creating value for, for you, our shareholders."

Garth Richie (00:38:54):

And obviously, um, you know, you end, you end up in a collective bargaining process with management. We think management, uh, David and his board were, and, and his VC partners, were incredibly adult and, and listened to us. Um, you know, there was obviously a, a, an arm wrestle what went into deep into the night, but we agreed that we felt that a billion pre-money was roughly right.

Garth Richie (00:39:16):

However, we then went further and said, uh, once we'd agreed on, uh, on a billion dollars, uh, pre-money, which you can see is a significant discount, we then said, "Look, David, we think that, uh, given that the growth that you will see and that we can see, we think that valuation should actually be at 900 million." And what we would do is on behalf of our shareholders, we would negotiate that and we would have an earn-out, that once the share price reached, um, 25% premium, um, and traded therefore at least 20 days in any 30, that what, that would happen is we would dilute ourselves and we'd give you back that 100 million in terms of valuation. Others would issue shares to you at $10.

Garth Richie (00:39:54):

Um, and thereby, we've aligned ourselves to everybody. Um, what the sponsors have done as well is they've locked

PART 2 OF 4 ENDS [00:40:04]

Garth Richie (00:40:03):

Themselves up on the same terms, um, that, uh, uh, as the earnout we're all aligned. And furthermore, I would say to you that in terms of the sponsorship, um, Manfredi Lefebvre, who is, um, our chairman, um, and who runs the Heritage Group, uh, has injected $50 million, um, into the pipe to cornerstone this transaction.

Garth Richie (00:40:21):

So therefore, you see that, that certainly we, we backed this with our money. Um, we backed it by saying that we'll lock ourselves up. We've done incredible due diligence on the company. Um, we feel, you know, very comfortable in recommending this to you, our shareholders, and we're happy to take any questions. Um, thank you very much for your time.

|

GMT20210818-170028_Recording (Completed 08/18/21) Transcript by Rev.com |

Page 11 of 24 |

This transcript was exported on Aug 19, 2021 - view latest version here.

John Yi (00:40:45):

Thank you, Garth. Ladies and gentlemen, at this time, as a reminder, if you'd like to ask a question, please submit your inquiry via the chat function. Again, if you have any questions you'd like to ask, please submit your inquiry via the chat function. David, our first question is, how do you feel about the minimum cash closing condition?

David Williams (00:41:06):

Ah, that's an interesting question. Well, one of the reasons for doing, uh, this SPAC transaction was that we felt that being a public company would deliver fantastic transparency to our customers.

David Williams (00:41:21):

Um, when you have transformational technology as we do, and to be clear, we firmly believe that Arqit has invented the most important cybersecurity technology of its generation, uh, it's really important that customers understand that that technology has been validated.

David Williams (00:41:39):