425: Filing under Securities Act Rule 425 of certain prospectuses and communications in connection with business combination transactions

Published on August 11, 2021

Filed by Arqit Quantum Inc.

Pursuant to Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

under the Securities Exchange Act of 1934

Subject Company: Centricus Acquisition Corp. (Commission File No. 001-39993)

Commission File No. for the Related Registration Statement: 333-256591

Arqit Stronger simpler encryption August 2021

2 Disclaimer (1/2) The following presentation, the information communicated during any delivery of the presentation and any question and answer ses sion and any other materials distributed at or in connection with the presentation (collectively, this “presentation”) has be en prepared by Arqit Quantum Inc. (“Arqit”) and Centricus Acquisition Corp. (“Centricus”) in connection with a proposed business combination betwe en Arqit and Centricus (the “Transaction”) and for no other purpose. This presentation may not be reproduced or distributed, in wh ole or in part. No Representations and Warranties This presentation is for informational purposes only and does not purport to contain all of the information that may be requi red to evaluate the Transaction. This presentation is not intended to form the basis of any investment decision and does not cons ti tute investment, tax or legal advice. No representation or warranty, express or implied, is or will be given by Arqit or Centricus or any of thei r r espective affiliates, directors, officers, employees or advisers or any other person as to the accuracy or completeness of th e i nformation in this presentation or any other written, oral or other communications transmitted or otherwise made available to any party in the c our se of its evaluation of a possible transaction between Arqit and Centricus and no responsibility or liability whatsoever is a cce pted for the accuracy or sufficiency thereof or for any errors, omissions or misstatements, negligent or otherwise, relating thereto. The informat ion contained in this presentation is preliminary in nature and is subject to change, and any such changes may be material. Arqit a nd Centricus disclaim any duty to update the information contained in this presentation. Viewers of this presentation should each make th eir own evaluation of Centricus, Arqit and the Transaction and of the relevant and adequacy of the information contained herein a nd should make such other investigations as they deem necessary. Forward - Looking Statements This presentation includes “forward - looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Arqit’s and Centricus’ actual results may differ from their expectations, e sti mates and projections and consequently, you should not rely on these forward - looking statements as predictions of future events. Words such as “expec t”, “estimate”, “project”, “budget”, “forecast”, “anticipate”, “intend”, “plan”, “may”, “will”, “could”, “should”, “believes” , “ predicts”, “potential”, “continue”, and similar expressions are intended to identify such forward - looking statements. These forward - looking statements include, without limitation, Arqit’s and Centricus’ expectations with respect to future performance and anticipated financial im pacts of the Transaction, the satisfaction of closing conditions to the Transaction and the timing of the completion of the Transaction. The se forward - looking statements involve significant risks and uncertainties that could cause the actual results to differ material ly from the expected results. Most of these factors are outside Arqit’s and Centricus’ control and are difficult to predict. Factors that may ca use such differences include, but are not limited to: (1) the outcome of any legal proceedings that may be instituted against Ar qi t or Centricus following the announcement of the Transaction; (2) the inability to complete the Transaction, including due to the inability to concurr ent ly close the business combination and the private placement of common stock or due to failure to obtain approval of the stock hol ders of Centricus; (3) delays in obtaining, adverse conditions contained in, or the inability to obtain necessary regulatory approvals or comple te regular reviews required to complete the Transaction; (4) the risk that the Transaction disrupts current plans and operations as a result of the announcement and consummation of the Transaction; (5) the inability to recognize the anticipated benefits of the Transaction, wh ich may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profit abl y, maintain relationships with customers and suppliers and retain its key employees; (6) costs related to the Transaction; (7) changes in th e applicable laws or regulations; (8) the possibility that the combined company may be adversely affected by other economic, bus iness, and/or competitive factors; (9) the impact of the global COVID - 19 pandemic: and (10) other risks and uncertainties indicated from time to time described in Centricus’ registration statement on Form S - 1, the proxy statement relating to the Transaction, including t hose under “Risk Factors” therein, and in Centricus’ other filings with the U.S. Securities and Exchange Commission (“SEC”). Arqit and Centric us caution that the foregoing list of factors is not exclusive and not to place undue reliance upon any forward - looking statements, including projections, which speak only as of the date made. Neither Arqit nor Centricus undertakes or accepts any obligation to relea se publicly any updates or revisions to any forward - looking statements to reflect any change in its expectations or any change in e vents, conditions or circumstances on which any such statement is based. Industry and Market Data In this presentation, Arqit and Centricus rely on and refer to publicly available information and statistics regarding market pa rticipants in the sectors in which Arqit competes and other industry data. Any comparison of Arqit to the industry or to any of its competitors is based on this publicly available information and statistics and such comparisons assume the reliability of the information availabl e t o Arqit. Arqit obtained this information and these statistics from third - party sources, including reports by market research fi rms and company filings. While Arqit believes such third - party information is reliable, there can be no assurance as to the accuracy or completeness of t he indicated information. Neither Arqit nor Centricus has independently verified the information provided by the third - party so urces. Trademarks This presentation may contain trademarks, service marks, trade names and copyrights of other companies, which are the propert y o f their respective owners. Solely for convenience, some of the trademarks, service marks, trade names and copyrights referre d t o in this presentation may be listed without the TM, SM © or © symbols, but Arqit and Centricus will assert, to the fullest extent unde r a pplicable law, the rights of the applicable owners, if any, to these trademarks, service marks, trade names and copyrights. No Offer or Solicitation This presentation does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitati on of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or s ale would be unlawful prior to the registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made exc ept by means a prospectus meeting the requirements of Section 10 of the Securities Act, or an exemption therefrom.

3 Disclaimer (2/2) Use of Projections This presentation also contains certain financial forecasts, including projected revenue, gross profit, EBITDA and unlevered fre e cash flow (“uFCF”) for Arqit’s fiscal years 2021 through 2025. Neither Centricus’ nor Arqit’s independent auditors have au dit ed, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, an d accordingly, neither of them expressed an opinion or provided any other form of assurance with respect thereto for the purp ose of this presentation, These projections are for illustrative purposes only and should not be relied upon as being necessarily indicat ive of future results. In this presentation, certain of the above - mentioned projected information has been provided for purposes o f providing comparisons with historical data. The assumptions and estimates underlying the prospective financial information are inheren tly uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that co ul d cause actual results to differ materially from those contained in the prospective financial information. Projections are inherently uncer tai n due to a number of factors outside of Centricus’ or Arqit’s control. Additionally, the projections are based on current bu sin ess plans and if new business plans are developed and/or implemented there is no assurance that the projections presented herein will be applicabl e. Accordingly, there can be no assurance that the prospective results are indicative of future performance of the combined comp an y after the Transaction or that actual results will not differ materially from those presented in the prospective financial information. In clusion of the prospective financial information in this presentation should not be regarded as a representation by any perso n t hat the results contained in the prospective financial information will be achieved. Use of Non - GAAP Financial Measures This presentation includes certain projections of non - GAAP financial measures, such as EBITDA (and related measures), and certai n ratios and other metrics derived therefrom. Arqit believes that these non - GAAP measures are useful to investors for two princ ipal reasons: 1) these measures may assist investors in comparing performance over various reporting periods on a consistent basis b y removing from operating results the impact of items that do not reflect core operating performance: and 2) these measures are used by Arqit’s management and board of directors to assess its performance and may (subject to the limitations described below) enab le investors to compare the performance of Arqit and the combined company to its competition. Arqit believes that the use of the se non - GAAP financial measures provides an additional tool for investors to use in evaluating ongoing operating results and trends. These n on - GAAP financial measures are not measures of financial performance in accordance with GAAP and may exclude items that are sign ificant in understanding and assessing Arqit’s financial results. Therefore, these non - GAAP measures should not be considered in isolation from, or as an alternative to, financial measures determined in accordance with GAAP. Due to the forward - looking nature of thes e non - GAAP financial measures, a reconciliation of non - GAAP financial measures in this presentation to the most directly comparable GAAP fi nancial measures is not included, because, without unreasonable effort, Arqit is unable to predict with reasonable certainty the amount or timing of non - GAAP adjustments that are used to calculate these forward - looking non - GAAP financial measures. The non - GAAP finan cial measures included in this presentation may not be comparable to similarly - titled measures presented by other companies. Ce rtain monetary amounts, percentages and other figures included in this presentation have been subject to rounding adjustments. Cert ain other amounts that appear in this presentation may not sum due to rounding. Additional Information Arqit has filed a proxy statement / prospectus with the SEC on Form F - 4 relating to the Transaction, which will be mailed to Cen tricus’ shareholders once definitive. This presentation does not contain all the information that should be considered concer nin g the Transaction and is not intended to form the basis of any investment decision or any other decision in respect of the Transaction. Centric us’ shareholders and other interested persons are advised to read, when available, the preliminary proxy statement / prospectus a nd the amendments thereto and the proxy statement / prospectus and other documents filed in connection with the Transaction, as thes e m aterials will contain important information about Arqit, Centricus, and the Transaction. When available, the proxy statement / p rospectus and other relevant materials for the Transaction will be mailed to shareholders of Centricus as of a record date to be establishe d f or voting on the Transaction. Shareholders will also be able to obtain copies of the preliminary proxy statement / prospectus , t he definitive proxy statement / prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.se c.g ov, or by directing a request to Arqit at 3 More London, London SE1 2RE or to Centricus at Centricus Acquisition Corp., Boun dar y Hall, Cricket Square, PO Box 1093, Grand Cayman KY1 - 1102, Cayman Islands. Participants in the Solicitation Centricus and its directors and executive officers may be deemed participants in the solicitation of proxies from Centricus’ sha reholders with respect to the Transaction. A list of the names of those directors and executive officers and a description of th eir interests in Centricus is contained in Centricus’ Registration Statement on Form S - 1, as effective on February 3, 2021, which was filed with the SEC and is available free of charge at the SEC’s web site at www.sec.gov, or by directing a request to Centricus at Centr icu s Acquisition Corp., Boundary Hall, Cricket Square, PO Box 1093, Grand Cayman KY1 - 1102, Cayman Islands. Additional information regarding the i nterests of such participants will be contained in the proxy statement / prospectus for the Transaction when available. Arqit and its directors and executive officers may also be deemed to be participants in the solicitation of proxies from the sha reholders of Centricus in connection with the Transaction. A list of the names of such directors and executive officers and i nfo rmation regarding their interests in the Transaction will be included in the proxy statement / prospectus for the Transaction when available.

4 Today’s presenters David Williams CEO and Founder, Arqit ▪ Former CEO & co - founder of Avanti plc ▪ Former TMT Banker ▪ Queens Award for Exports 2016 Garth Ritchie CEO, Centricus Acquisition Corp ▪ Former Head of Investment Bank for Deutsche Bank and Member of Management Board ▪ Joined Centricus in June 2020 ▪ Over 25 years of experience in banking and finance

Centricus Acquisition Corporation overview 5 ▪ Centricus Acquisition Corporation (NASDAQ: CENHU) is a Nasdaq - listed blank check company led by former executives at Silversea Cruises and Centricus ▪ This entity was formed by Centricus and Heritage Group: ▪ Monaco - based private equity group with a core focus / expertise on travel and leisure, technology as well as medical / BioTech companies ▪ London - based global investment firm, overseeing $30bn of assets and targeting returns in four core sectors: Financial services, Technology, Infrastructure and CMES (1) ▪ In February 2021, the company priced an upsized IPO worth $345m by offering 34.5m units at $10.00 per unit Defensible market position in large / growing markets x Compelling upside unlocked through their operational expertise x Forefront of shifting technological and consumer landscapes x Ranging from $1bn – 3bn in transaction value x Garth Ritchie CEO Over 25 years of experience in banking and finance, most recently as the Head of Investment Bank for Deutsche Bank until July 2019, and member of the Board from January 2016. Joined Centricus in June 2020 Manfredi Lefebvre d’Ovidio Chairman Chairman of Heritage Group, and also Executive Chairman from 2001 to 2020 for Silversea Cruises, expanding the company from a cruise line with three vessels to covering over 900 destinations globally Appointed CIO of Heritage Group in 2019, serving as the Managing Director of Silversea Expeditions, Vice Chairman of Abercrombie & Kent, and Chairman of Bucksense Independent director with Altair Partners Limited since May 2018. From October 1994 to June 2017, Nicholas Taylor served at Ashburton Investments, initially as Finance Director before becoming CFO and COO ¹ Consumer, Media, Entertainment and Sports; Source: Company information Cristina Levis CFO, CIO, Secretary Nicholas Taylor Board of Directors Highly experienced management Well defined acquisition criteria Business at a glance

Vision Our mission is to use our world leading quantum encryption platform to keep safe the data of our governments, enterprises and citizens. 6 Arqit’s quantum tech stack allows lightweight end point software to create encryption keys which are computationally secure, zero trust and one time in infinite numbers and infinite group sizes. We already taking the software to market at pace.

Problem: legacy encryption is obsolete 7 ▪ PKI was designed decades ago ▪ It was never intended to protect our hyper connected world ▪ It has many vulnerabilities in its implementation for attackers to exploit ▪ Quantum computers will soon compromise the mathematics at the heart of PKI ▪ The world is being urged to create and adopt new protections ▪ The efforts to make PKI more resistant to quantum attack are temporary, and pose grave problems in usability “We need to determine where, why, and with what priority vulnerable public - key algorithms will need to be replaced, and we need to understand the constraints that apply to specific use cases. These initial steps in developing and implementing algorithm migration playbooks can and should begin immediately.” National Institute of Science and Technology, U.S. Department of Commerce, April 28 th 2021

8 Solution: A new way to distribute symmetric encryption keys Arqit transformational innovation A completely new way to create and distribute unbreakable symmetric keys Symmetric keys are the solution Long random number cannot be broken by computers Used with physical couriers for decades Previously not possible to distribute them electronically with adequate security Suitable for hyper scale Software, fulfilled from the cloud, automatically creates keys in infinite volumes at minimal cost. Solves the problem for every connected device in the world Simple to implement The keys are used in a global standard algorithm that is already widely used called AES256

“Arqit is paving the way in developing a new generation of quantum technologies that defend against sophisticated cyber - attacks on national governments”. - UK Government Minister for Science, Amanda Solloway MP “ We are proud to be providing this technology to UK customers, which will bolster our industry - leading security capabilities.” - Howard Watson, Chief Technology Officer of BT “an opportunity to contribute enhancement of cyber security capabilities for the important benefit of Japanese governments, e nte rprises and citizens.” - Eiji Ishida, Executive Officer and General Manager, Sumitomo Corporation “With the support of the Canadian government, we have been pleased to be associated with Arqit's commercial mission … which w ill further the collective security goals of the ‘Five Eyes’ community of nations”. Marina Mississian, Senior Director Honeywell “Arqit ... a key element of Leonardo’s strategy to establish and deliver next generation systems to our customers enabling ef fec tive and secure multi - domain operations including in the cyber and space domains”. - Norman Bone, Chair and Managing Director, Leonardo UK “Leveraging our U.S. expertise related to market access for quantum encryption technology has the potential to add significan t v alue to our customer solutions.” Nick Chaffey, Chief Executive of Northrop Grumman UK, Europe and Middle East “.. a ground - breaking approach to legal innovation that has given us an opportunity to shape the next generation of KYC and complian ce software.” Dr Justin Hill, Partner at Dentons 9 What are Customers Saying ?

10 Transatlantic leadership in cloud encryption David Bestwick CTO & Founder Former CTO, Avanti plc. Marconi engineer. Astrophysicist. Royal Aeronautical Society medal winner Dr Daniel Shiu Chief Cryptographer Former Head of Mathematics & National Technical Authority for Cryptographic Design & Quantum Information Processing, GCHQ Inventor of SSL, Security CTO Sales Force, Operating Partner, Evolution Equity Partners Dr Taher Elgamal Director, Arqit Ltd Former Engineering Director, McAfee UK Enterprise Data Protection David Webb Chief Engineer Former Deputy Chief of Staff for Intelligence, Surveillance, Reconnaissance, and Cyber Effects Operations, U.S. Air Force General VeraLinn Jamieson Director, Arqit Inc Former Chief of Research and Innovation, GCHQ and the Deputy Chief Scientific Advisor for National Security Daryl Burns Inventor, Consultant Former Group CISO, HSBC & CTO, Cisco. PhD Cryptography. Fellow Royal Academy of Engineering Dr Alison Vincent Adviser 44 years’ experience since winning the IBM prize aged 13 specialising in High Performance Computing Dr Barry Childe Chief Innovation officer Former Chief Executive, GCHQ Sir Iain Lobban Adviser Formerly 22 Years a Main Board Director at GCHQ. PhD in Quantum Molecular Dynamics Dr Geoffrey Taylor, CB Co - Founder, Adviser David Williams CEO & Founder Former CEO & Co - Founder, Avanti plc. TMT Banker. Queens Award for Exports 2016 Nick Pointon CFO Former CFO, Privitar. Ex VP Finance, King Digital. KPMG ACA Former four - star Vice Chief of Staff of the US Air Force. Retired 2020 Gen Seve Wilson Director, Arqit Inc Air Vice Marshal RAF Capability, highly decorated aviator & military leader Air Vice Marshal Rocky Rochelle CB COO Former Director, Jumo World and Avanti Government Services. British Army Officer who led the UK’s Counter Terrorism Planning for 2012 Olympic Games Paul Feenan Chief Revenue Officer Formerly of IBM and Hewlett Packard. PhD in Post Quantum Cryptography Stephen Holmes Chief Product Officer

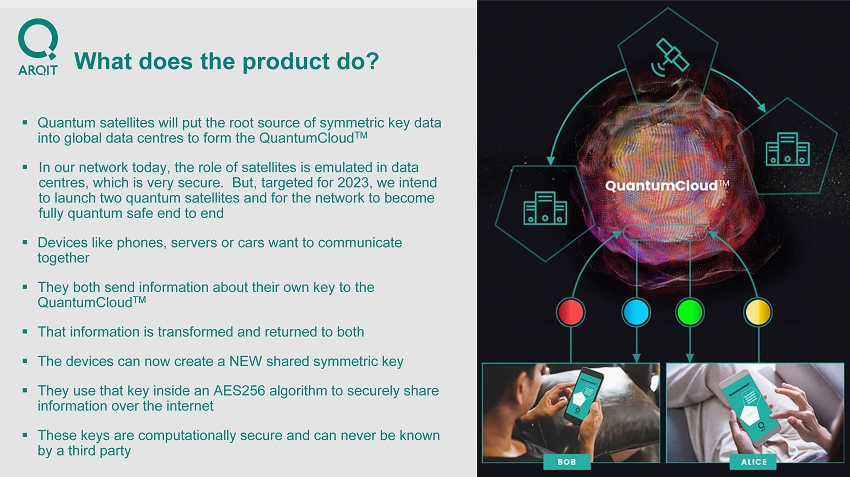

11 What does the product do? ▪ Quantum satellites will put the root source of symmetric key data into global data centres to form the QuantumCloud TM ▪ In our network today, the role of satellites is emulated in data centres, which is very secure. But, targeted for 2023, we intend to launch two quantum satellites and for the network to become fully quantum safe end to end ▪ Devices like phones, servers or cars want to communicate together ▪ They both send information about their own key to the QuantumCloud TM ▪ That information is transformed and returned to both ▪ The devices can now create a NEW shared symmetric key ▪ They use that key inside an AES256 algorithm to securely share information over the internet ▪ These keys are computationally secure and can never be known by a third party

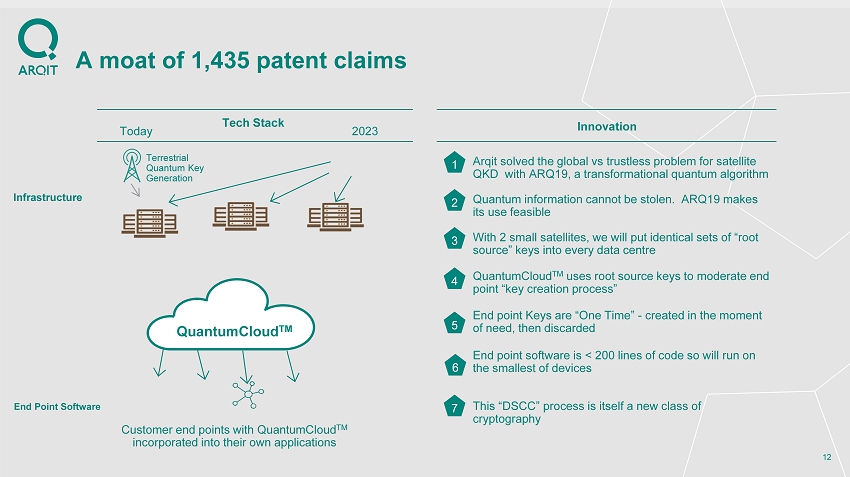

A moat of 1,435 patent claims 12 Today Innovation Arqit solved the global vs trustless problem for satellite QKD with ARQ19, a transformational quantum algorithm 1 4 QuantumCloud TM uses root source keys to moderate end point “key creation process” 5 End point Keys are “One Time” - created in the moment of need, then discarded 6 Customer end points with QuantumCloud TM incorporated into their own applications QuantumCloud TM Quantum information cannot be stolen. ARQ19 makes its use feasible 2 Infrastructure End Point Software With 2 small satellites, we will put identical sets of “root source” keys into every data centre 3 This “DSCC” process is itself a new class of cryptography 7 Terrestrial Quantum Key Generation Tech Stack 2023 End point software is < 200 lines of code so will run on the smallest of devices

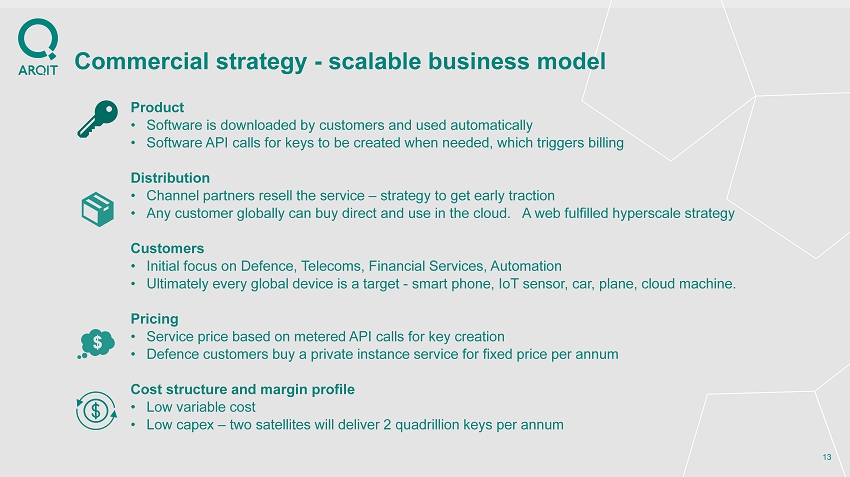

Commercial strategy - scalable business model 13 Product • Software is downloaded by customers and used automatically • Software API calls for keys to be created when needed, which triggers billing Distribution • Channel partners resell the service – strategy to get early traction • Any customer globally can buy direct and use in the cloud. A web fulfilled hyperscale strategy Customers • Initial focus on Defence, Telecoms, Financial Services, Automation • Ultimately every global device is a target - smart phone, IoT sensor, car, plane, cloud machine. Pricing • Service price based on metered API calls for key creation • Defence customers buy a private instance service for fixed price per annum Cost structure and margin profile • Low variable cost • Low capex – two satellites will deliver 2 quadrillion keys per annum

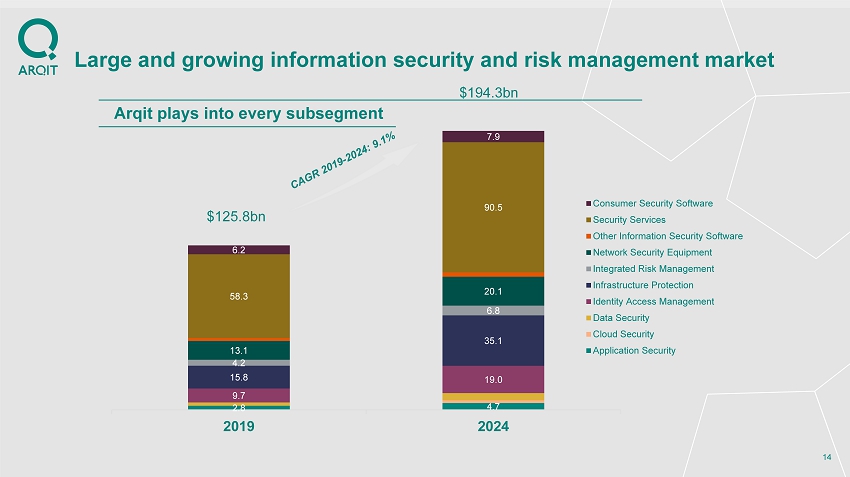

Large and growing information security and risk management market 14 Arqit plays into every subsegment $125.8bn $194.3bn 2.8 4.7 9.7 19.0 15.8 35.1 4.2 6.8 13.1 20.1 58.3 90.5 6.2 7.9 2019 2024 Consumer Security Software Security Services Other Information Security Software Network Security Equipment Integrated Risk Management Infrastructure Protection Identity Access Management Data Security Cloud Security Application Security

Early distribution strategy backed by blue - chip partners Tech applies to every vertical in the World, but early Customers secured in key vertical markets 15 Defence Telco Financial Services Automation Making fixed and 5G networks end to end secure. Securing the future battlespace. Connected cars. Smart cities. Global payment networks. Identity. Blockchain. BP Major payment network Government of UK

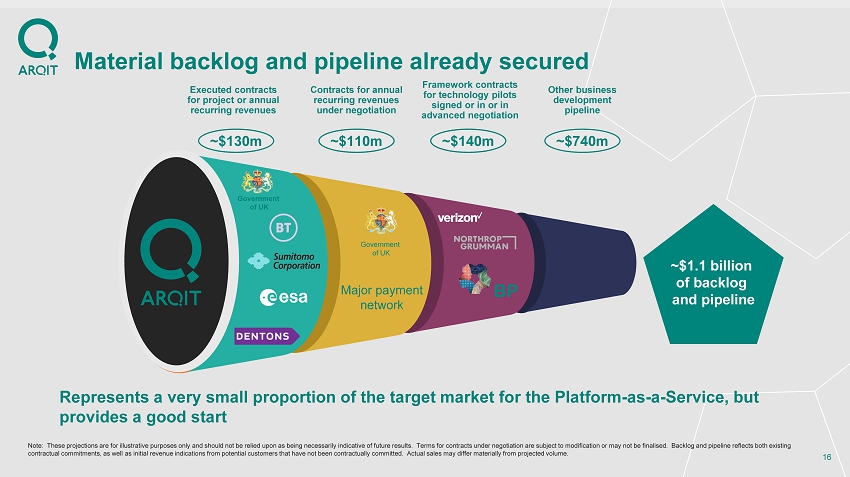

Material backlog and pipeline already secured 16 Government of UK Government of UK ~$1.1 billion of backlog and pipeline ~$130m ~$110m ~$140m ~$740m Executed contracts for project or annual recurring revenues Contracts for annual recurring revenues under negotiation Framework contracts for technology pilots signed or in or in advanced negotiation Other business development pipeline Note: These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of fut ure results. Terms for contracts under negotiation are subject to modification or may not be finalised. Backlog and pipeline r eflects both existing contractual commitments, as well as initial revenue indications from potential customers that have not been contractually com mit ted. Actual sales may differ materially from projected volume. BP Represents a very small proportion of the target market for the Platform - as - a - Service, but provides a good start Major payment network

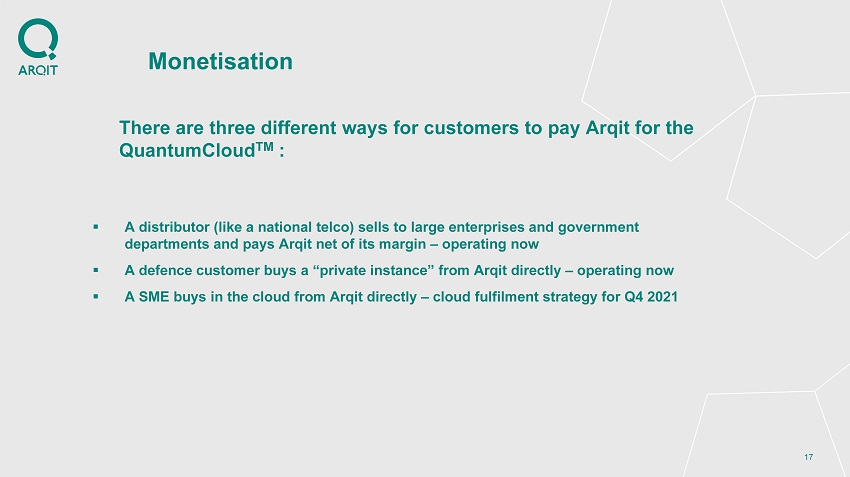

17 Monetisation ▪ There are three different ways for customers to pay Arqit for the QuantumCloud TM : ▪ A distributor (like a national telco) sells to large enterprises and government departments and pays Arqit net of its margin – operating now ▪ A defence customer buys a “private instance” from Arqit directly – operating now ▪ A SME buys in the cloud from Arqit directly – cloud fulfilment strategy for Q4 2021

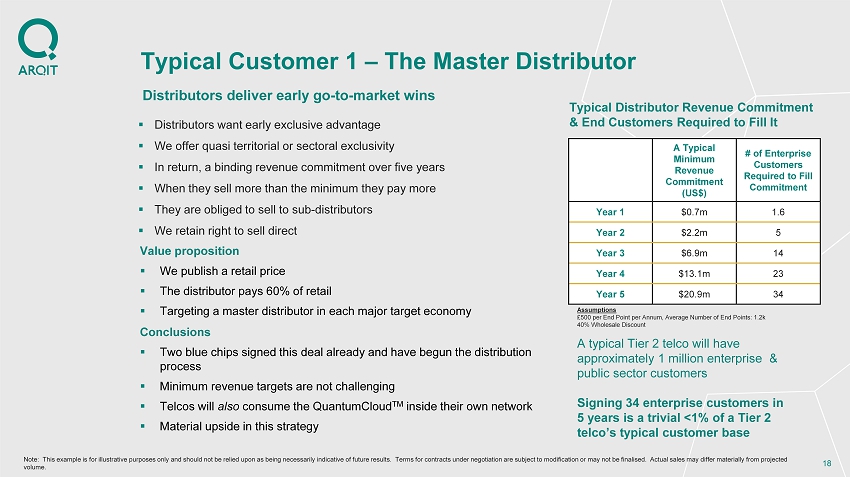

Distributors deliver early go - to - market wins 18 Typical Customer 1 – The Master Distributor ▪ Distributors want early exclusive advantage ▪ We offer quasi territorial or sectoral exclusivity ▪ In return, a binding revenue commitment over five years ▪ When they sell more than the minimum they pay more ▪ They are obliged to sell to sub - distributors ▪ We retain right to sell direct Value proposition ▪ We publish a retail price ▪ The distributor pays 60% of retail ▪ Targeting a master distributor in each major target economy A Typical Minimum Revenue Commitment (US$) # of Enterprise Customers Required to Fill Commitment Year 1 $0.7m 1.6 Year 2 $2.2m 5 Year 3 $6.9m 14 Year 4 $13.1m 23 Year 5 $20.9m 34 Assumptions £500 per End Point per Annum, Average Number of End Points: 1.2k 40% Wholesale Discount A typical Tier 2 telco will have approximately 1 million enterprise & public sector customers Signing 34 enterprise customers in 5 years is a trivial <1% of a Tier 2 telco’s typical customer base Conclusions ▪ Two blue chips signed this deal already and have begun the distribution process ▪ Minimum revenue targets are not challenging ▪ Telcos will also consume the QuantumCloud TM inside their own network ▪ Material upside in this strategy Typical Distributor Revenue Commitment & End Customers Required to Fill It Note: This example is for illustrative purposes only and should not be relied upon as being necessarily indicative of future re sults. Terms for contracts under negotiation are subject to modification or may not be finalised. Actual sales may differ mate rially from projected volume.

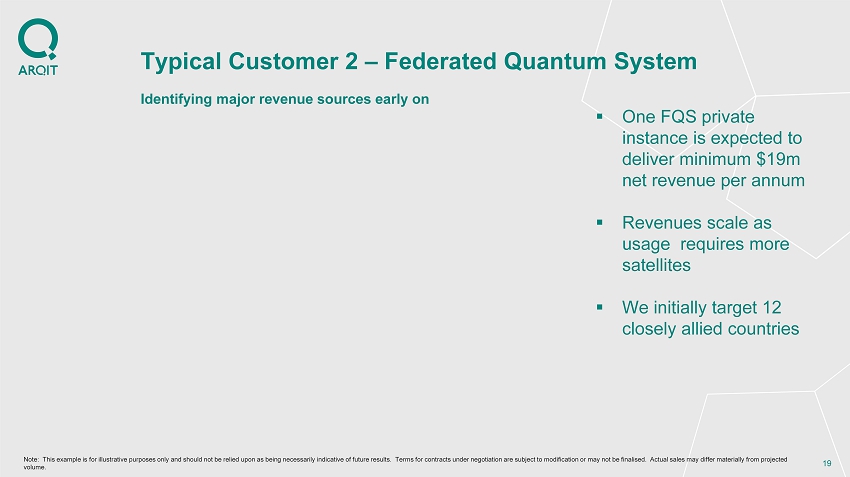

Identifying major revenue sources early on 19 Typical Customer 2 – Federated Quantum System ▪ One FQS private instance is expected to deliver minimum $19m net revenue per annum ▪ Revenues scale as usage requires more satellites ▪ We initially target 12 closely allied countries Note: This example is for illustrative purposes only and should not be relied upon as being necessarily indicative of future re sults. Terms for contracts under negotiation are subject to modification or may not be finalised. Actual sales may differ mate rially from projected volume.

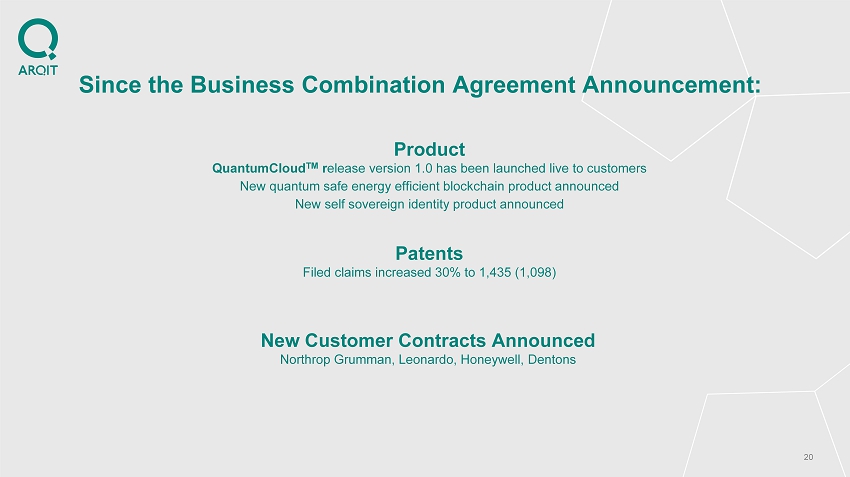

20 Since the Business Combination Agreement Announcement: Patents Filed claims increased 30% to 1,435 (1,098) Product QuantumCloud TM r elease version 1.0 has been launched live to customers New quantum safe energy efficient blockchain product announced New self sovereign identity product announced New Customer Contracts Announced Northrop Grumman, Leonardo, Honeywell, Dentons

Financial and Transaction Overview

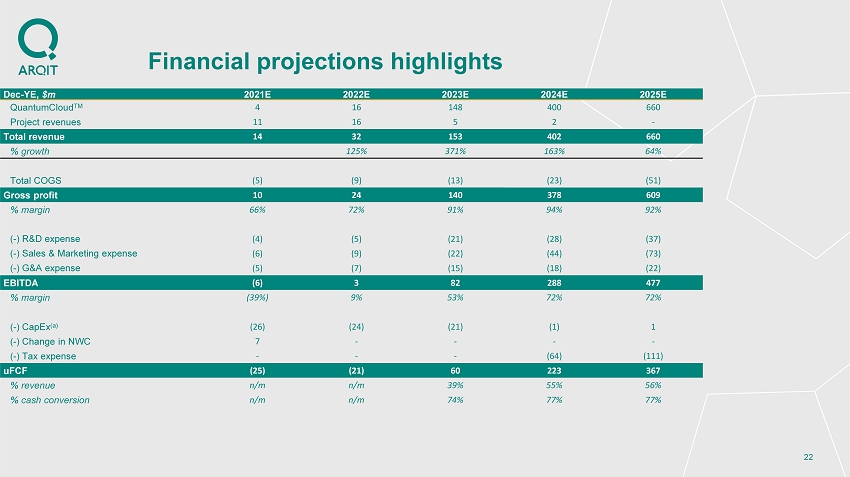

22 Financial projections highlights Dec - YE, $ m 2021E 2022E 2023E 2024E 2025E Quantum Cloud TM 4 16 148 400 660 Project revenues 11 16 5 2 - Total r evenue 14 32 153 402 660 % growth 125% 371% 163% 64% Total COGS (5) (9) (13) (23) (51) Gross profit 10 24 140 378 609 % margin 66% 72% 91% 94% 92% ( - ) R&D expense (4) (5) (21) (28) (37) ( - ) Sales & Marketing expense (6) (9) (22) (44) (73) ( - ) G&A expense (5) (7) (15) (18) (22) EBITDA (6) 3 82 288 477 % margin (39%) 9% 53% 72% 72% ( - ) CapEx (a) (26) (24) (21) (1) 1 ( - ) Change in NWC 7 - - - - ( - ) Tax expense - - - (64) (111) uFCF (25) (21) 60 223 367 % revenue n/m n/m 39% 55% 56% % cash conversion n/m n/m 74% 77% 77%

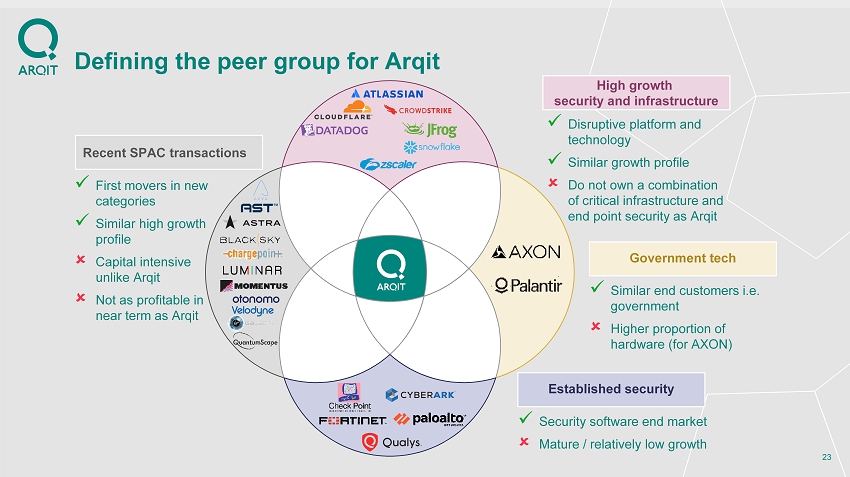

Defining the peer group for Arqit 23 x First movers in new categories x Similar high growth profile Capital intensive unlike Arqit Not as profitable in near term as Arqit Recent SPAC transactions Established security x Security software end market Mature / relatively low growth Government tech x Similar end customers i.e. government Higher proportion of hardware (for AXON) High growth security and infrastructure x Disruptive platform and technology x Similar growth profile Do not own a combination of critical infrastructure and end point security as Arqit

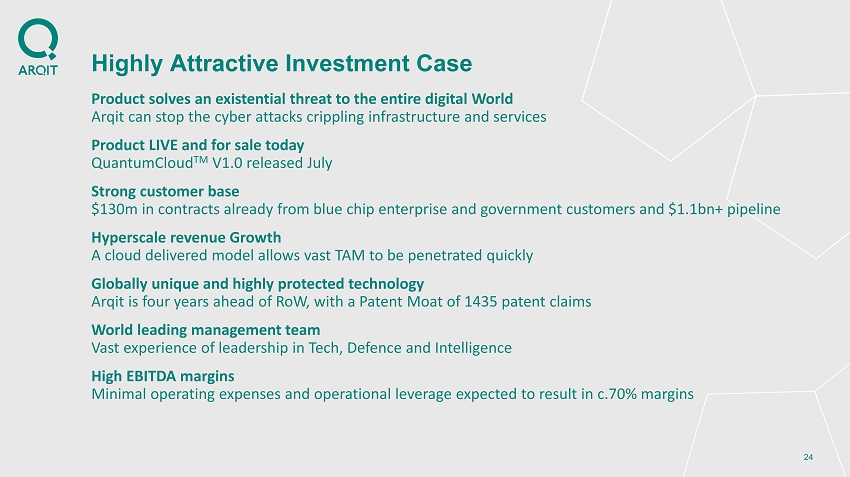

24 Highly Attractive Investment Case Product solves an existential threat to the entire digital World Arqit can stop the cyber attacks crippling infrastructure and services Product LIVE and for sale today QuantumCloud TM V1.0 released July Strong customer base $130m in contracts already from blue chip enterprise and government customers and $1.1bn+ pipeline Hyperscale revenue Growth A cloud delivered model allows vast TAM to be penetrated quickly Globally unique and highly protected technology Arqit is four years ahead of RoW, with a Patent Moat of 1435 patent claims World leading management team Vast experience of leadership in Tech, Defence and Intelligence High EBITDA margins Minimal operating expenses and operational leverage expected to result in c.70% margins

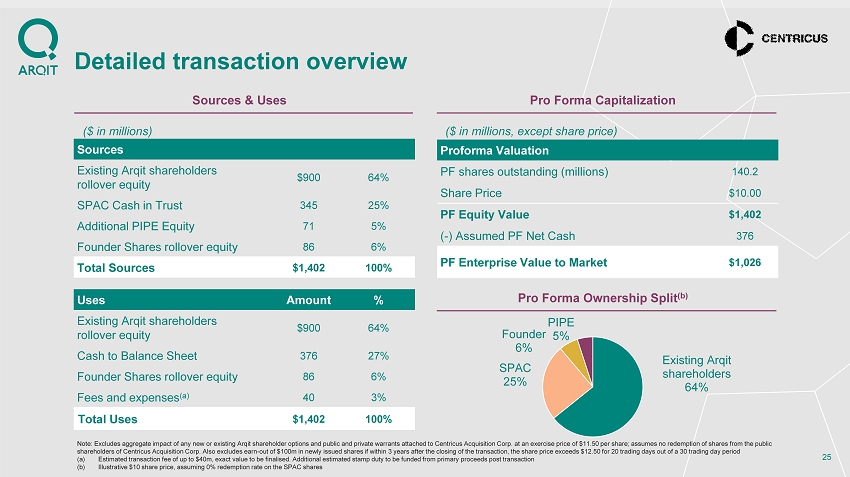

Detailed transaction overview 25 Sources & Uses Pro Forma Capitalization ($ in millions) Sources Amount % Existing Arqit shareholders rollover equity $900 64% SPAC Cash in Trust 345 25% Additional PIPE Equity 71 5% Founder Shares rollover equity 86 6% Total Sources $1,402 100% Uses Amount % Existing Arqit shareholders rollover equity $900 64% Cash to Balance Sheet 376 27% Founder Shares rollover equity 86 6% Fees and expenses (a) 40 3% Total Uses $1,402 100% Proforma Valuation Amount PF shares outstanding (millions) 140.2 Share Price $10.00 PF Equity Value $1,402 ( - ) Assumed PF Net Cash 376 PF Enterprise Value to Market $1,026 Pro Forma Ownership Split (b) Note: Excludes aggregate impact of any new or existing Arqit shareholder options and public and private warrants attached to Cen tricus Acquisition Corp. at an exercise price of $11.50 per share; assumes no redemption of shares from the public shareholders of Centricus Acquisition Corp. Also excludes earn - out of $100m in newly issued shares if within 3 years after the c losing of the transaction, the share price exceeds $12.50 for 20 trading days out of a 30 trading day period (a) Estimated transaction fee of up to $40m, exact value to be finalised. Additional estimated stamp duty to be funded from prima ry proceeds post transaction (b) Illustrative $10 share price, assuming 0% redemption rate on the SPAC shares ($ in millions, except share price) Existing Arqit shareholders 64% SPAC 25% Founder 6% PIPE 5%

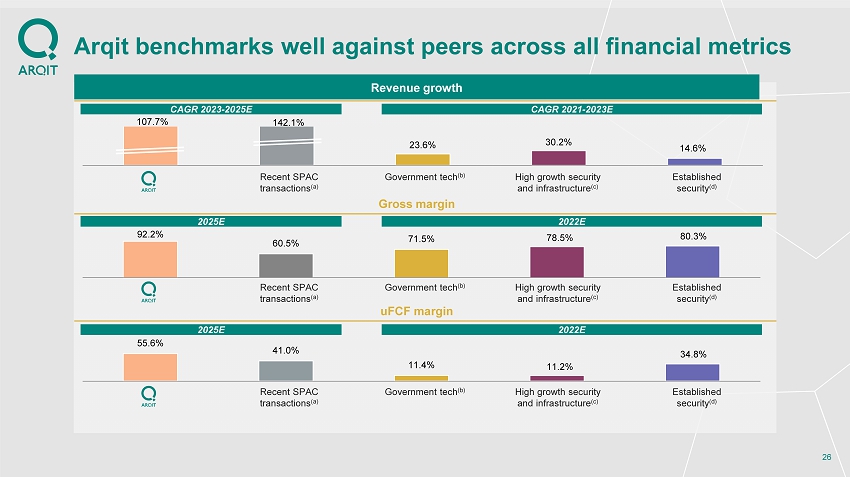

107.7% 142.1% 23.6% 30.2% 14.6% Arqit benchmarks well against peers across all financial metrics 26 Revenue growth Gross margin uFCF margin High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) CAGR 2023 - 2025E CAGR 2021 - 2023E 2025E 2022E 2025E 2022E 92.2% 60.5% 71.5% 78.5% 80.3% 55.6% 41.0% 11.4% 11.2% 34.8%

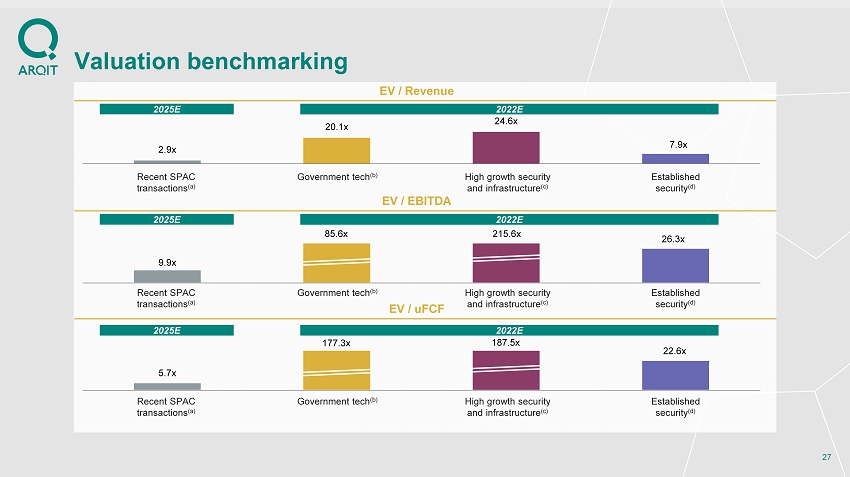

5.7x 177.3x 187.5x 22.6x 9.9x 85.6x 215.6x 26.3x Valuation benchmarking 27 EV / Revenue EV / EBITDA EV / uFCF High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) High growth security and infrastructure (c) Government tech (b) Recent SPAC transactions (a) Established security (d) 2025E 2022E 2025E 2022E 2025E 2022E 2.9x 20.1x 24.6x 7.9x

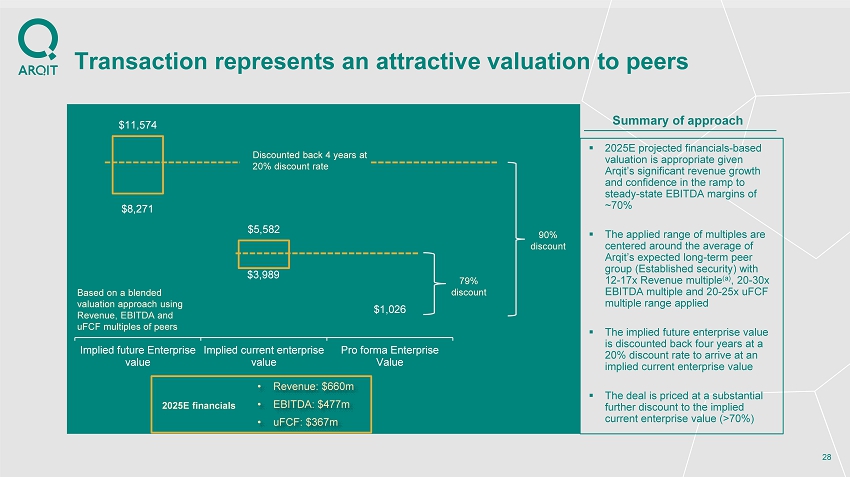

$8,271 $3,989 $1,026 $11,574 $5,582 Implied future Enterprise value Implied current enterprise value Pro forma Enterprise Value Transaction represents an attractive valuation to peers 28 ▪ 2025E projected financials - based valuation is appropriate given Arqit’s significant revenue growth and confidence in the ramp to steady - state EBITDA margins of ~70% ▪ The applied range of multiples are centered around the average of Arqit’s expected long - term peer group (Established security) with 12 - 17x Revenue multiple (a) , 20 - 30x EBITDA multiple and 20 - 25x uFCF multiple range applied ▪ The implied future enterprise value is discounted back four years at a 20% discount rate to arrive at an implied current enterprise value ▪ The deal is priced at a substantial further discount to the implied current enterprise value (>70%) Based on a blended valuation approach using Revenue, EBITDA and uFCF multiples of peers Discounted back 4 years at 20% discount rate 79% discount 90% discount • Revenue: $660m • EBITDA: $477m • uFCF: $367m 2025E financials Summary of approach

Additional Materials Benchmarking

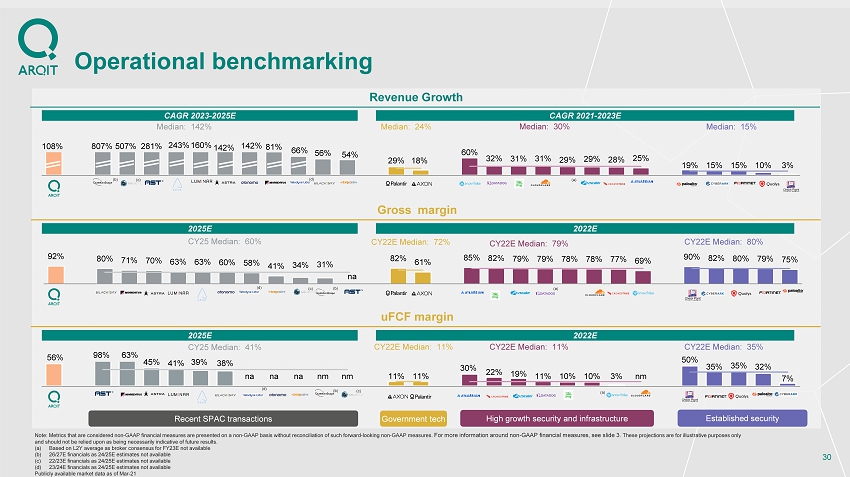

92% 80% 71% 70% 63% 63% 60% 58% 41% 34% 31% na 82% 61% 85% 82% 79% 79% 78% 78% 77% 69% 90% 82% 80% 79% 75% CY22E Median: 79 % CY25 Median: 60% CY22E Median: 80% CY22E Median: 72% 56% 98% 63% 45% 41% 39% 38% na na na nm nm 11% 11% 30% 22% 19% 11% 10% 10% 3% nm 50% 35% 35% 32% 7% CY22E Median: 11% CY25 Median: 41% CY22E Median: 35% CY22E Median: 11% 108% 807% 507% 281% 243% 160% 142% 142% 81% 66% 56% 54% 29% 18% 60% 32% 31% 31% 29% 29% 28% 25% 19% 15% 15% 10% 3% Median: 30% Median: 15 % Median: 24 % Median: 142 % Operational benchmarking 30 CAGR 2023 - 2025E CAGR 2021 - 2023E High growth security and infrastructure Established security Recent SPAC transactions Government tech Revenue Growth Gross margin uFCF margin 2025E 2022E 2025E 2022E (b) (c) (a) (b) (c) (a) Note: Metrics that are considered non - GAAP financial measures are presented on a non - GAAP basis without reconciliation of such f orward - looking non - GAAP measures. For more information around non - GAAP financial measures, see slide 3. These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. (a) Based on L2Y average as broker consensus for FY23E not available (b) 26/27E financials as 24/25E estimates not available (c) 22/23E financials as 24/25E estimates not available (d) 23/24E financials as 24/25E estimates not available Publicly available market data as of Mar - 21 (b) (c) (a) (d) (d) (d)

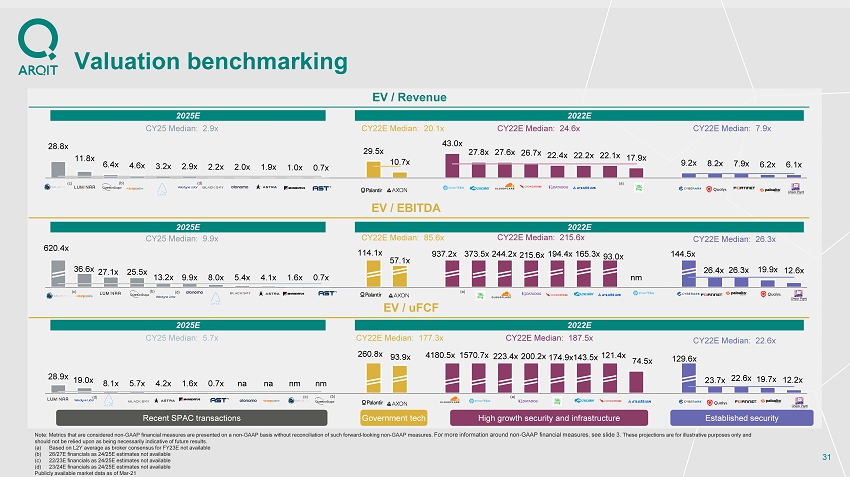

620.4x 36.6x 27.1x 25.5x 13.2x 9.9x 8.0x 5.4x 4.1x 1.6x 0.7x 114.1x 57.1x 937.2x 373.5x 244.2x 215.6x 194.4x 165.3x 93.0x nm 144.5x 26.4x 26.3x 19.9x 12.6x CY25 Median: 9.9x CY22E Median: 26.3x CY22E Median: 85.6x CY22E Median: 215.6x 28.9x 19.0x 8.1x 5.7x 4.2x 1.6x 0.7x na na nm nm 260.8x 93.9x 4180.5x 1570.7x 223.4x 200.2x 174.9x 143.5x 121.4x 74.5x 129.6x 23.7x 22.6x 19.7x 12.2x CY22E Median: 22.6x CY25 Median: 5.7x CY22E Median: 177.3x CY22E Median: 187.5x 28.8x 11.8x 6.4x 4.6x 3.2x 2.9x 2.2x 2.0x 1.9x 1.0x 0.7x 29.5x 10.7x 43.0x 27.8x 27.6x 26.7x 22.4x 22.2x 22.1x 17.9x 9.2x 8.2x 7.9x 6.2x 6.1x CY25 Median: 2.9x CY22E Median: 24.6x CY22E Median: 7.9x CY22E Median: 20.1x Valuation benchmarking 31 EV / Revenue EV / uFCF EV / EBITDA High growth security and infrastructure Established security Recent SPAC transactions Government tech 2025E 2022E 2025E 2022E 2025E 2022E (b) (c) (a) (b) (c) (a) (b) (c) (a) Note: Metrics that are considered non - GAAP financial measures are presented on a non - GAAP basis without reconciliation of such f orward - looking non - GAAP measures. For more information around non - GAAP financial measures, see slide 3. These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. (a) Based on L2Y average as broker consensus for FY23E not available (b) 26/27E financials as 24/25E estimates not available (c) 22/23E financials as 24/25E estimates not available (d) 23/24E financials as 24/25E estimates not available Publicly available market data as of Mar - 21 (d) (d) (d)

Investor Deck Transcript

Monday 9 August | Presented by David Williams and Garth Ritchie

Garth Ritchie:

Hello , I am Garth Ritchie. I am the Chief Executive Officer of Centricus Acquisition Corp. Our Board has unanimously recommended a merger with Arqit. Centricus Acquisition Corp raised $345 million via an IPO earlier this year. We have also secured $71 million of committed financing via a PIPE. These funds will be injected into the merged entity, to fund hyper growth of Arqit.

The merger application to the SEC has been approved and the transaction has now been deemed effective.

As a sponsor group, we're incredibly enthused by the opportunity that we believe Arqit will be delivering to our shareholders, so much so, that our chairman, Manfredi Lefebvre, has invested $50million through the PIPE vehicle into this transaction. We are so excited to bring this to you, our shareholders. Without further ado, I’d like to hand over to David, who is the Founder and Chief Executive of Arqit. David –

David Williams:

Thank you, Garth and welcome to this presentation. I am very excited to be working with the Centricus team, particularly Garth, who led one of the world’s biggest investment banks as its Chief Executive and Manfredi Lefebvre, who is one of Europe’s most successful entrepreneurs, of the recent decade.

Arqit’s mission is to use our world leading quantum encryption platform to keep safe the data of our governments, enterprises, and citizens. Arqit’s quantum tech stack allows lightweight end point software to create encryption keys which are computationally secure, zero trust and one time, in infinite numbers and infinite group sizes. We’re already taking the software to market at pace.

The problem we solve is that legacy encryption is already obsolete. PKI was designed decades ago. It was never intended to protect our hyper connected world. It has many vulnerabilities in its implementation which attackers are currently exploiting, with ransomware and malware attacks that hit the headlines almost daily. Quantum computers will also make that situation worse in coming years when the mathematics at the heart of PKI, is definitively destroyed.

The world is being urged to create and adopt new protections but the efforts to make PKI more resistant to quantum attack are temporary and pose grave problems in usability. That’s why in April this year, the National Institute for Science and Technology of the U.S Department of Commence stated that it’s of fundamental importance that steps to develop and implement brand new algorithmic playbooks, should begin immediately. This problem is a clear and urgent and pressing problem that the world must embrace with great urgency.

The solution is to be found in symmetric encryption keys. Arqit didn’t invent symmetric encryption keys; they’ve been used for many decades. What Arqit has invented, is a brand-new way to securely distribute them. We know that symmetric encryption keys (which are just long, random numbers that are shared by two or more parties) can never be broken, even by future quantum computers. Previously, these keys have been distributed by physical couriers; it hasn't been possible to distribute them with adequate security electronically.

So, Arqit’s transformational innovation is a completely new way to create and distribute unbreakable symmetric encryptions keys and because they've been used for many decades, these keys are used inside a globally standardised algorithm that's already widely used, baked into most of the worlds networking software systems called AES256. The software is delivered from the cloud, and it automatically creates keys in high volume and minimal cost. It can solve the problem for every connected device in the world and that means that the Arqit business is now suitable for hyperscale growth.

I thought it would be a good idea to let you know what customers are saying. We recently announced that the QuantumCloud™ product is live for service and we already have over $130 million of signed committed revenue contracts but take a look at what our customers are saying about our products.

- The British Government, a big supporter since the very beginning, have said that we’re paving the way in developing a new generation of technologies that defend against sophisticated attacks on national governments.

- British Telecom, which has also been a very strong partner since the beginning of our business in 2017, declared that they are proud to be using this technology and providing it to UK customers, to bolster their own industry leading security capabilities.

- Sumitomo, a very strong partner in Japan, are looking forward to contributing to the enhancement of cyber security capabilities for the benefit of the Japanese Government, enterprises, and citizens.

- In Honeywell we have a partner which is pleased to be making strong additions to the collective security goals of the ‘Five Eyes’ community of nations.

- With Leonardo, an Anglo-Italian defence business, we know that Arqit’s technology is becoming a key element of their strategy to establish and deliver next generation systems to their customers to enable effective and secure multi domain operations, including in the cyber and space domains.

- Northrop Grumman, one of the world's greatest Defence primes, believes that leveraging their own US expertise in relation to market access for our quantum encryption technology, has the potential to add very significant value to their existing customer solutions.

- And, with Dentons, we've invented what they regard to be a ground-breaking approach to legal innovation that has given them the opportunity to shape the next generation of KYC and compliance software.

So, customers are using the Arqit products today and they are universally finding it to be an important part of their technology future.

How did this happen? The innovation is very comprehensive across the domains of physics, crypto mathematics and IT and the most important elements of our company are the people. The Co-Founders with me and David Bestwick in this business, include four former directors and senior managers of the British cyber intelligence agency, GCHQ. Our full time Chief Cryptographer, Dr Daniel Shiu was formerly the National Technical Authority in Great Britain for Cryptographic Design and Quantum Information Processing. My co-founder Dr Geoffrey Taylor was on the main board of GCHQ for 22 years and Daryl Burns as Chief of Research and Innovation at GCHQ occupied the seat once occupied by Alan Turing, the inventor of the computer. And we’re fortunate to be advised by Sir Ian Lobban, who was Chief Executive at GCHQ.

On the transatlantic side of our business, Dr Tahir Elgamal is recognised by those of us who know the cyber security industry as ‘the godfather of cyber security’, he invented SSL, the technique which underpins most e-commerce cyber security that we use today. General Seve Wilson was formerly the four-star Vice Chief of the United States Air Force and working alongside him in that period was -General VeraLinn Jamieson, who was three star General, was the Deputy Chief of Staff for Intelligence and Cyber Warfare. Seve and VeraLinn give Arqit incredible credentialising effect in the United States market. And Dave Webb, our Chief Software Engineer was formerly the engineering director for McAfee Enterprise Data Protection Software, so has been at the heart of some of the most important endpoint software developments over the last couple of decades.

Also in banking, Dr Vincent, a PhD cryptographer herself, was Head of Global Security at HSBC and Dr Barry Childe was its Chief Innovation Officer.

I believe we have the most impressive bench of technicians and scientists of any cyber security start up, that I’ve ever seen.

So, what does the QuantumCloud™ product do? The product that is in the market today being sold to and used by customers today. Effectively, a small piece of software, a lightweight software agent consisting of no more than 200 lines of code, is downloadable from the cloud to any form of device (it could be an IoT sensor, a phone, a laptop, a server, a router or a fighter jet). It's the same piece of software regardless of the application and device.

The software is able to talk to the Arqit QuantumCloud™ which brokers conversations with other devices and those devices, which all have the Arqit software either embedded in them or built on a white label basis into other companies’ apps, the QuantumCloud™ talks to that software and brokers the creation of a brand new key. So, brand new symmetric encryption keys are created locally at endpoint devices. The QuantumCloud™ doesn't know the key, it's simply sending clues about how to create a key to the endpoint devices .

QuantumCloud™ is able to do this because at its heart, it has identical HSM's which are computers which store keys in every data centre, participating in the network globally. Currently these ‘root source keys’ as we call them, are distributed using a terrestrial method which is regarded as very secure but in two years’ time, Arqit will launch quantum encryption satellites. These satellites are able to put identical copies of symmetric encryption keys into all of the data centres in the world, in a manner which is described as quantum safe. So, that means it is impossible for any third party ever to intercept, know or use those root source keys. So, today we have a product which is live in the market which is very secure and in two years’ time the entire tech stack gets upgraded with the use of quantum satellites. That means that our end-to-end system will be fully quantum safe before a quantum computer arrives.

The keys, once they’re created at the local endpoint software are then simply used inside the standard AES256 algorithm, to encrypt and decrypt data which the parties share across the regular internet. There are three things about these keys which are important. Firstly, because they're symmetric encryption keys, they are what's known as computationally secure. That means they can never be broken by any form of computer including quantum computers deep into the future. Secondly they’re trustless or zero trust. That means that no third party ever knows the key or has enough information to guess the key, even the servers inside the Arqit QuantumCloud™ never have enough information to guess the key. Finally, the keys are one time. They are not in existence before an API call is made. Only when our customers decide that they want to use a key, is the key created. The key is created, used once, and then discarded, so the key is never lying around waiting for a bad guy to be able to find it. The ability to create keys which are one time, zero trust, and computationally secure is the holy grail of cyber security and there is no other organisation has been ever, ever able to produce a network which achieves those three things in its product.

Arqit spent almost five years inventing this technology and now has a moat of 1435 patent claims protecting this tech from the space infrastructure, the protocols, into the data centres and down to the QuantumCloud™ endpoint software. We believe that that patent moat is likely to give the company and its investors very significant protection from emerging competition for a period of quite some years.

So, the commercial strategy of the company makes this a very scalable business model. The product is just a small piece of software, that can be downloaded by customers from the cloud and used automatically. When an API call is made for keys to be created, a billing event is triggered. The software ultimately will be sold to all accredited and qualifying customers in the cloud but initially we have a distribution strategy that involves some distribution channel partners and some customer direct business and the initial focus on customers has been in Defence, Telecoms, Financial Services and Automation but to that we've very recently added a new focus on Blockchain. Ultimately, we believe that every global device is a target for this service, whether it's a smartphone, a cloud machine, or an aircraft.

Pricing never appears to be a barrier to sale for us. The service price is based on metered API calls for key creation and we’re able to price bundles of keys so that this product can cost a few dollars a year or millions of dollars a year, depending on the scale of the endpoint devices that customers want to use. And, finally, because the CapEx involved in launching two very small satellites is very low, this is a incredibly powerful business model with low variable cost and low CapEx. With the root source keys that we create with just two satellites, the QuantumCloud™ can deliver 2 quadrillion keys per annum. So, this is unlikely to be a business that will need to consume significant cash in future.

We think of the TAM as the entire information security market because everything that anyone does in IT, data communications, and cyber security, must have strong encryption at its heart. The commercial IT security market is expected to rise to about $200 billion by 2024/5, but this does not include markets like Defence, the connected car, many IoT markets.

So, our strategy to demonstrate our technology was all about finding early customers to validate our assumptions and we focused initially on four sectors. In telecommunications, we were blessed to be partnered from the very beginning by British Telecom, who have been a fantastic partner and signed a very significant multiyear revenue contract with us a few months ago. We're also working on demonstrating the product in 5G networks with our friends Verizon and in terrestrial infrastructure with Juniper Networks.

In the government market, the Government of the United Kingdom has given us very large multiple 10s of millions of dollars contracts in the last few years but also Sumitomo Corporation of Japan signed a multiyear, very large contract with us to buy our service and sell it to the Japanese Government, which we announced earlier this year. And then we were recently joined by Northrop Grumman, who are taking this product to market in a very large customer base focused on Defence. Others, like Leonardo, have recently announced their participation in some of our programmes.

In financial services we’re working with one very large payment network and we recently announced the work that we're doing with the largest law firm in the world Dentons, to secure the future of identity. We have some very interesting partnerships with BP, the energy company, and NEOM the smart city project in the Kingdom of Saudi Arabia. These projects are largely about automation.

We have announced recently a new focus on Blockchain technology. We believe that Blockchain has an important future for many parts of the global economy but that this potential cannot be realised until the PKI cyber security problem at the heart of Blockchain is solved. We've demonstrated that new forms of public key algorithms so called ‘Post Quantum Algorithms’ render Blockchains impossible to operate efficiently. We believe that Arqit’s QuantumCloud™ service is the solution for the Blockchain of the future.

We've demonstrated that Post Quantum Algorithms are 1400 times slower than the Arqit QuantumCloud™ and therefore you’re going to hear quite a lot more from us, I believe, in the coming months about what Arqit can do for Blockchain applications in things like Smart Cities, Central Bank Digital Currencies, supply chains, and alternative cryptocurrencies.

As a result of that early work, we've already secured a backlog of over $130 million of binding revenue commitments and a pipeline of over $1 billion of potential projects.

So, a few words on monetisation, how do we take this product to market and how do we turn it into cash? There are three methods of selling our product. 1) Through a distributor like a national telco, who buys the product and sells it on to large enterprises and government customers. 2) In Defence. We announced recently at the G7 conference a project called FQS which stands for the Federated Quantum System, whereby direct Defence customers buy what's known as a private instance from Arqit directly. Finally, 3) any form of customer which is properly accredited will be able to buy the Arqit QuantumCloud™ product directly with a cloud fulfilment strategy that will be testing in quarter four of this year and deploying at scale next year.

So, a worked example of a typical customer a master distributor. Distributors like telecoms companies find the product very appealing for use in their own networks but also to sell through to end user customers. Most telecoms companies are finding that cyber security is now between 5 and 10% of their global revenue base and that number is growing very fast and therefore securing a degree of exclusivity over Arqit’s product is regarded as attractive. A typical distributor, which might be a telco in a medium sized company, will make a legally binding commitment to pay Arqit approximately $1 million in the first year of contract, rising to approximately $20 million in the fifth year of the contract and they have to pay that whether they use it or not.

However, that commitment is regarded as very small. A typical medium sized company telco, will have over one million enterprise customers. If they only signed 34 average enterprise customers, they would fully satisfy their year five commitment. Therefore, the revenues that we’re locking in from these distribution agreements does not represent, in my opinion, a strong percentage of the likely revenue that we can get from these distribution agreements, but it does provide strong validation that Arqit’s product is highly valued by significant telecoms and other distribution partner companies.

Our second typical customer is representing that Federated Quantum System. We found that Defence department customers observed that whilst it's true that Arqit can never know the keys that are being created, the typical Defence department customer for various reasons connected with physical security, doesn't wish to outsource fully their long-term encryption creation process and therefore we were asked to develop a product called ‘a private instance’. So, Arqit builds a turnkey version of the system called a private instance and sells it to the defence department customer who therefore has an entirely private end to end instance of this technology. Arqit continues to provide long term software upgrades and support and training and the typical customer pays to Arqit, net of the cost of delivering the private instance, approximately $19 million of revenue per annum.

At the recent G7 conference, we announced that six countries and their service provider representatives have joined the FQS project. The British Government has already signed the first contract for FQS, other governments are now joining the project to validate the technology and we expect those other governments also to go to full scale revenue commitments and I hope you'll be hearing from Arqit very soon with more information on the trajectory of that project, which will provide, if successful, very strong underpinning for the cash flow forecast of the company.

So, we announced the business combination agreement with Centricus only approximately six months ago. Since then, we've made very dramatic strides in all areas of the business. When we made the business combination announcement, we said that we expected to fully release the first version of QuantumCloud™ to the market by December 2021. We in fact launched the product in July, well ahead of schedule. Testing with customers was very successful and the product is now live and available for testing and integration with a large number of customers, in fact we already had 20 live engagements where customers are receiving, testing and integrating the software.

We also announced that Arqit has created a new quantum safe and energy efficient Blockchain product and there will be more discussion on the importance of this to the Blockchain community in the coming weeks and months.

We also announced a self-sovereign identity product. We believe that identity is at the heart of everything that humans and machines must do on the Internet and we're very focused on making that product a big success.

We’ve continued to file more patent claims. The number of filed patent claims increased by 30% in the period from 1098 to 1435.

We also announced significant new customer contracts with Northrop Grumman, Leonardo, Honeywell and Dentons on top of the contracts with British Telecom and Sumitomo, which we announced in the first week after the business combination agreement was announced.

So, the investment case for Arqit is incredibly strong. The product solves an existential threat for the entire digital world and it's live and for sale today. We have a strong customer base with over $130 million of revenue contracts and with a cloud delivered model, the company is ready for hyperscale growth. The technology is globally unique and highly protected, and it's being delivered by a world leading management team and that we believe delivers a product and a technology with very high cash flow margins. These are represented in the financial projections here. We believe that if we only sell distribution agreements to half of the 30 NATO countries that we’re targeting and if we only sell FQS instances to half of the 30 NATO countries that we’re targeting, that we will achieve our revenue forecast by 2025. But that also doesn't include the potential that we could realise from selling the cloud delivered model to the mass market of smaller medium sized enterprises globally.

As you can see, because CapEx is very low, the revenue turns into positive cash flow quite quickly. Most of the invention is done and therefore R&D doesn't need to consume an enormous part of our cash flow and sales and marketing expenses largely geared to commercial success in signing contracts with customers.

And, just finally, a quick word on defining the peer group for Arqit. There are many excellent cyber security companies that have come to the public markets and remain private in recent years, delivering an excellent level of a new style of cloud delivered service and we believe that these are the companies that were most closely associated with. But, all of those companies have PKI encryption at the heart of their services. We believe that most of these cyber security companies are not competitors to Arqit; we believe that they are potential partners (as we found with companies like BT which is a major cyber security provider).

Arqit has found a way to replace and upgrade PKI encryption with a new form of distributing symmetric encryption keys and those keys can be baked into virtually any cloud delivered software system. So, whereas Arqit is unique in finding a new way of distributing symmetric encryption keys, we believe that we will take to market a very collaborative approach, where we can add value to the rich cyber security services that are provided by the latest generation of cloud service companies.

On the transaction overview, I'll invite Garth to offer a few comments on his view of the transaction and its valuation.

Garth Ritchie:

I think David has discussed the benefits that Arqit will bring to the market more broadly. What we did is we focused, as I mentioned earlier, on contracts, on the technology and on the customer roll out and once we looked at that and we had a backdrop of valuation in the market, we believe (as the slide that David has been talking through demonstrate) that we have secured a compelling valuation for our shareholders by any metric and therefore we continue to be incredibly excited about the prospects for this company going forward.

David Williams:

That brings to an end our presentation for today. Thank you very much for engaging and we look forward to talking more with all of our shareholders in future.

Garth Ritchie:

Thank you

---End---

Additional Information

Arqit has filed a proxy statement / prospectus with the SEC on Form F-4 relating to the Transaction, which has been mailed to Centricus’ shareholders. This presentation does not contain all the information that should be considered concerning the Transaction and is not intended to form the basis of any investment decision or any other decision in respect of the Transaction. Centricus’ shareholders and other interested persons are advised to read the definitive proxy statement / prospectus and the amendments thereto and other documents filed in connection with the Transaction, as these materials will contain important information about Arqit, Centricus, and the Transaction. The proxy statement / prospectus and other relevant materials for the Transaction have been mailed to shareholders of Centricus as of July 26, 2021, the record date established for voting on the Transaction. Shareholders are also be able to obtain copies of the preliminary proxy statement / prospectus, the definitive proxy statement / prospectus and other documents filed with the SEC, without charge at the SEC’s website at www.sec.gov, or by directing a request to Arqit at 3 More London, London SE1 2RE or to Centricus at Centricus Acquisition Corp., Boundary Hall, Cricket Square, PO Box 1093, Grand Cayman KY1-1102, Cayman Islands.

Participants in the Solicitations

Arqit, Centricus and certain of their respective directors, executive officers and other members of management and employees may, under SEC rules, be deemed to be participants in the solicitation of proxies from Centricus’ shareholders in connection with the proposed transaction. Information about Centricus’ directors and executive officers and their ownership of Centricus’ securities will be set forth in the proxy statement/prospectus when available. Additional information regarding the participants in the proxy solicitation and a description of their direct and indirect interests will be included in the proxy statement/prospectus when it becomes available. Shareholders, potential investors and other interested persons should read the proxy statement/prospectus carefully when it becomes available before making any voting or investment decisions. You may obtain free copies of these documents from the sources indicated above.

No Offer or Solicitation

This communication does not constitute an offer to sell or the solicitation of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offering of securities shall be made except by means of a prospectus meeting the requirements of section 10 of the Securities Act, or an exemption therefrom.

Caution About Forward-Looking Statements

This communication includes forward-looking statements. These forward-looking statements are based on Arqit’s and Centricus’s expectations and beliefs concerning future events and involve risks and uncertainties that may cause actual results to differ materially from current expectations. These factors are difficult to predict accurately and may be beyond Arqit’s and Centricus’s control. Forward-looking statements in this communication or elsewhere speak only as of the date made. New uncertainties and risks arise from time to time, and it is impossible for Arqit and Centricus to predict these events or how they may affect Arqit and Centricus. Except as required by law, neither Arqit and Centricus has any duty to, and does not intend to, update or revise the forward-looking statements in this communication or elsewhere after the date this communication is issued. In light of these risks and uncertainties, investors should keep in mind that results, events or developments discussed in any forward-looking statement made in this communication may not occur. Uncertainties and risk factors that could affect Arqit’s and Centricus’s future performance and cause results to differ from the forward-looking statements in this release include, but are not limited to: (i) that the business combination may not be completed in a timely manner or at all, which may adversely affect the price of Centricus’ securities, (ii) the risk that the business combination may not be completed by Centricus’ business combination deadline and the potential failure to obtain an extension of the business combination deadline if sought by Centricus, (iii) the failure to satisfy the conditions to the consummation of the business combination, including the approval of the Business Combination Agreement by the shareholders of Centricus and the satisfaction of the minimum trust account amount following any redemptions by Centricus’ public shareholders, (iv) the lack of a third-party valuation in determining whether or not to pursue the business combination, (v) the occurrence of any event, change or other circumstance that could give rise to the termination of the Business Combination Agreement, (vi) the effect of the announcement or pendency of the business combination on the Company’s business relationships, operating results, and business generally, (vii) risks that the business combination disrupt current plans and operations of the Company, (viii) the outcome of any legal proceedings that may be instituted against the Company or against Centricus related to the Business Combination Agreement or the business combination, (ix) the ability to maintain the listing of Centricus’ securities on a national securities exchange, (x) changes in the competitive and regulated industries in which the Company operates, variations in operating performance across competitors, changes in laws and regulations affecting the Company’s business and changes in the combined capital structure, (xi) the ability to implement business plans, forecasts, and other expectations after the completion of the business combination, and identify and realize additional opportunities, (xii) the potential inability of the Company to convert its pipeline or orders in backlog into revenue, (xiii) the potential inability of the Company to successfully deliver its operational technology which is still in development, (xiv) the potential delay of the commercial launch of the Company’s products, (xv) the risk of interruption or failure of the Company’s information technology and communications system and (xvi) the enforceability of the Company’s intellectual property.